To view this presentation in PDF format, click here.

Finanzplaner – Tagung der Schweiz 2014

The Armageddon of the 21st Century

March 25, 2014

Jonathan Lachowitz CFP®

Financial Planner – Investment Advisor

This presentation is not meant as legal, tax or financial advice to any individual. You are strongly recommended to seek the advice of a professional who understands your specific circumstances before relying on any of the information in this presentation. There may be mistakes and regulations may change or not apply in some circumstances. The presentation may be circulated but should be appropriately cited if used in a professional setting.

IRS Circular 230 Disclosure: Any tax advice in this communication is not intended or written by the author to be used, and cannot be used, by a client or any other person or entity for the purpose of avoiding penalties that may be imposed on any taxpayer.

FATCA Agenda

A Brief History

New Language Common Definitions

American Taxpayers – Clients

Swiss Independent Asset Managers

Other Swiss FFIs

Registering a Swiss IAM

US-Swiss IGA

Timeline

Consultants

Future of FATCA

Useful Links

Armageddon - The Last Battle of Good vs Evil Before the Day of Judgement

Who is responsible? Who is good vs who is evil?

Max Bacus (D) - Former US Senator from Montana - Now Ambassador to China

Charles Rangel (D) - US Representative from New York’s 13th District

Timothy Geithner - Former US Treasury Secretary 2009-2013

Doug Shulman - Former Commissioner of IRS 2008-2012

US President Barak Obama - Do you think FATCA would have passed under President Bush?

Marcel Rohner - UBS - Former CEO UBS 2007-2009 and former CEO Wealth Management

Brady Dougan - Current CEO - Credit Suisse

Bradley Birkenfeld - Former UBS banker turned whistleblower…multimillionaire etc…[released from prison Aug 1, 2012]

American Tax Cheats - Unfortunately lumped into some basket with all overseas Americans with non-US accounts

Swiss Banks & Banking Secrecy - Secrecy is good - breaking laws or aiding others to break laws in other countries is not good

A Brief History

The Foreign Account Tax Compliance Act (FATCA), introduced as part of the HIRE Act and enacted into law by the 111th Congress. onMarch 18, 2020 is designed to compel foreign financial institutions (FFIs) and non-financial foreign entities (NFFEs) to provide information to the US Internal Revenue Service (IRS) about US persons who old accounts with or interests in FFIs and NFEEs.

FATCA was meant to combat offshore tax evasion and to recoup federal tax revenues.

Under US tax law, US persons are generally required to report and pay taxes on income from all sources regardless of where they live.

The IRS previously instituted a Qualified Intermediary (QI) program under Internal Revenue Code §1441 which required participating foreign institutions to maintain records of the US or foreign status of their account holders and to report income and withhold taxes. One report found that participation in the QI program was too low to have substantive impacts as an enforcement measure and was prone to abuse: [As has been demonstrated by UBS and Credit Suisse as well as the relatively small number of Overseas Americans filing tax returns and FBARS.]

3 Primary FATCA Provisions

It requires foreign financial institutions (FFIs) to enter into an agreement with the IRS to identify their US account holders. and periodically disclose the account holders’ names, TINs, addresses, and the accounts’ balances, receipts, and withdrawals.

US payers making payments to non-compliant foreign financial institutions are required to withhold 30% of the gross payments. Foreign financial institutions which are themselves the beneficial owners of such payments are not permitted a credit or refund or refund on withheld taxes absent a treaty override

US persons owning these foreign accounts or other specified financial assets must report them on a new Form 8938 which is filed with the person’s US tax returns if the accounts are generally worth more than US$50,000; a higher reporting threshold applies to overseas residents and others

Account holders would be subject to a 40% penalty on understatements of income in an undisclosed foreign financial asset. Understatements of greater than 25% of gross income are subject to an extended statute of limitations period of 6 years. It also requires taxpayers to report financial assets that are not held in a custodial account, i.e., physical stock or bond certificates.

It closes a tax loophole that foreign investors had used to avoid paying taxes on US dividends by converting them into “dividend equivalent” through the use of swap contracts

These reporting requirements are in addition to the requirement for reporting of foreign financial accounts to the US Treasury; [27] this most notably includes Form TD 90-22.1 [Now FinCEN114] “Report of Foreign Bank and Financial Accounts” (FBAR) for foreign financial accounts exceeding US $10,000 required under Bank Secrecy Act [28] regulations issued by the Financial Crimes Enforcement Network (FinCEN).

New Language – Common Definitions

Foreign Financial Institution (FFI):

Any financial institution that is a foreign entity. The list includes, but is not limited to banks, insurance companies, many but not all trusts, investment advisors (even if they don’t hold custody of client assets), holding company, treasury center, collective investment vehicle, entities that make commercial loans, an entity that buys or sells accounts receivable, provides trust or fiduciary services, finances foreign exchange, etc. (The actual definition is many pages long and has some exceptions.) It is a project for most entities just to determine if they are an FFI.

New Language

There are many categories of FFIs including: Deemed Compliant FFis, Certified Deemed Compliant FFIs, Registered Deemed Compliant FFIs and Owner Documented FFIs each with its own particular definition and requirements.

Registered Deemed Compliant Procedural Requirements: The final regulations provide a registered deemed-compliant FFI with six months from the time it becomes ineligible for the registered deemed-compliant status to cure the default or notify the IRS of its change in status.

Non-Participating FFI: The term non-participating FFI means an FFI other than a participating FFI, a deemed-compliant FFI, or an exempt beneficial owner.

Non-Reporting IGA FFI: The term non-reporting IGA FFI means an FFI that is identified a non-reporting financial institution pursuant to a Model 1 IGA or Model 2 IGA that is not a registered deemed-compliant FFI.

Non-Financial Foreign Entity (NFFE) means a foreign entity that is not a financial institution

Sponsoring Entity: The term sponsoring entity means an entity that registers with the IRS and agrees to perform the due diligence, withholding, and reporting obligations or one or more FFIs.

Sponsored FFIs: The term sponsored FFI group means a group of sponsored Foreign Financial Institutions whose shared sponsoring entity is responsible for the FATCA reporting and the compliance of all underlying FFIs. [e.g. If a Trust company is the sponsor of all the trust where it acts as a Trustee.]

Non-Participating FFI: This essentially means all non-US financial institutions other than FFIs or deemed compliant FFIs.

FFI Agreement: An agreement between a Foreign Financial Institution and the IRS that will require the FFI to collect certain information on their clients and in many cases to report annual information to the IRS as well as withhold US taxes on certain US income and other payments. [It has been noted that the IRS will not be able to perform on sight compliance audits of Swiss FFIs thought it appears that they may request this type of assistance from the Swiss government.]

Model I & II Inter Governmental Agreements (IGAs): The US Treasury department has collaborated with other governments to develop two alternative model intergovernmental agreements to facilitate the implementation of FATCA; primarily by removing legal impediments to data reporting cross borders.

Countries that sign and use the Model 1 agreement [First published on July 26, 2012] will have their FFIs report information directly to their home government about US accounts and account holders, and that government will report the information to the IRS on an automatic basis.

Countries that sign and use the Model 2 agreement [first published on November 14, 2012] will direct and enable their FFIs to report information directly to the IRS. In this agreement, there still will be room for government to government exchanges.

The IRS is hoping to conclude over 50 signed agreements in the near future, though to date less than ten have been signed with the Swiss agreement being one of the first.

IRS Reviews: The IRS may make general inquiries to FFIs requesting additional information regarding information reported (on Forms 1042, 1042-S, 8966 or additional annual reporting that may be required in the future) on a regular basis to the IRS. If an FFI has been found to be non-compliant with the FFI agreement, the IRS will allow an FFI to develop a plan to come into compliance rather than immediately suspending the FFI.

Specified United States Person: A specified US person is generally a US citizen, US resident or for other reasons a person (or entity) that is liable for US taxes; though there are many exceptions for entities. Companies that are regularly traded in the public markets; organizations exempt from US taxes, entities of the US Federal or State governments or any sub division. See page 499 for more details.

Recalcitrant Account Holders: The account holder fails to comply with requests by the FFI for the documentation or information that is required under for determining the status of such account as a US account or other than a US account. [The definition goes on for many pages, this is a brief summary.]

Withholdable Payment: Any payment of US source FDAP (fixed or determinable annual or periodic) income. Also includes and is not limited to: Investment advisory fees, custodial fees, bank and brokerage fees, payments in connection with lending transactions, amounts paid under cash value insurance or annuity contracts, dividends, interest, interest on outstanding accounts payable, etc.

Withholding Taxes: FATCA imposes a 30% withholding tax on certain US-source payments (and payments of gross proceeds from the disposition of property that can produce such payments) made to an FFI unless the FFI enters into an agreement with the IRS to report the identities and other information about its US account holders. FATCA also requires FFIs that enter into such agreements (participating FFIs) to withhold 30% of “pass thru payments” made to other FFIs that do not comply with the FATCA rules. FATCA requires NFFEs to report information about their substantial US holders to paying Agents in order to avoid 30% withholding tax.

FATCA Registration Portal: FFIs registering with the IRS will be able to do so through an on-line portal designed to accommodate a paperless registration process. It is expected that the Portal, will be available no later than July 15, 2013. [Though it appears that annual reporting will be done on “magnetic media” and possibly through electronic files; which seems quite a burden for those entities that may have only a few US account holders and no withholding to report and submit.]

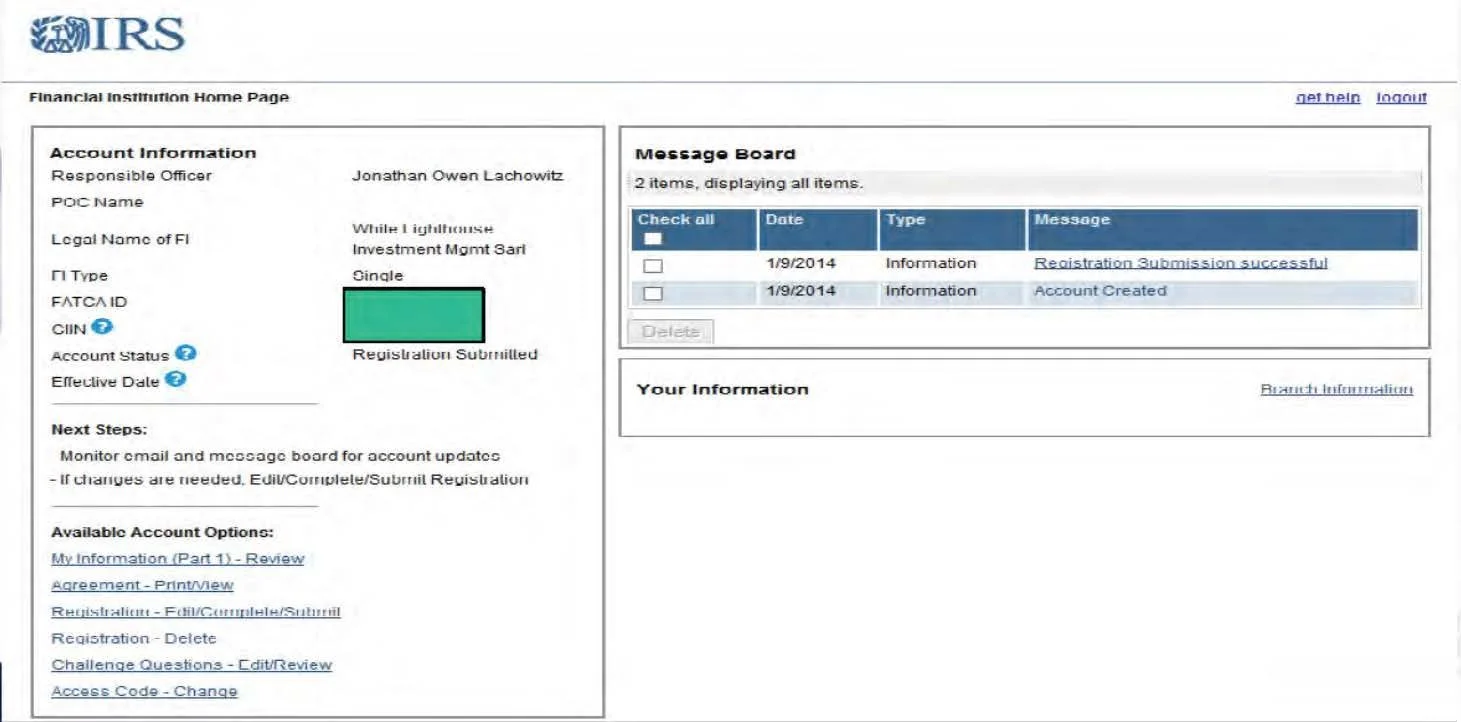

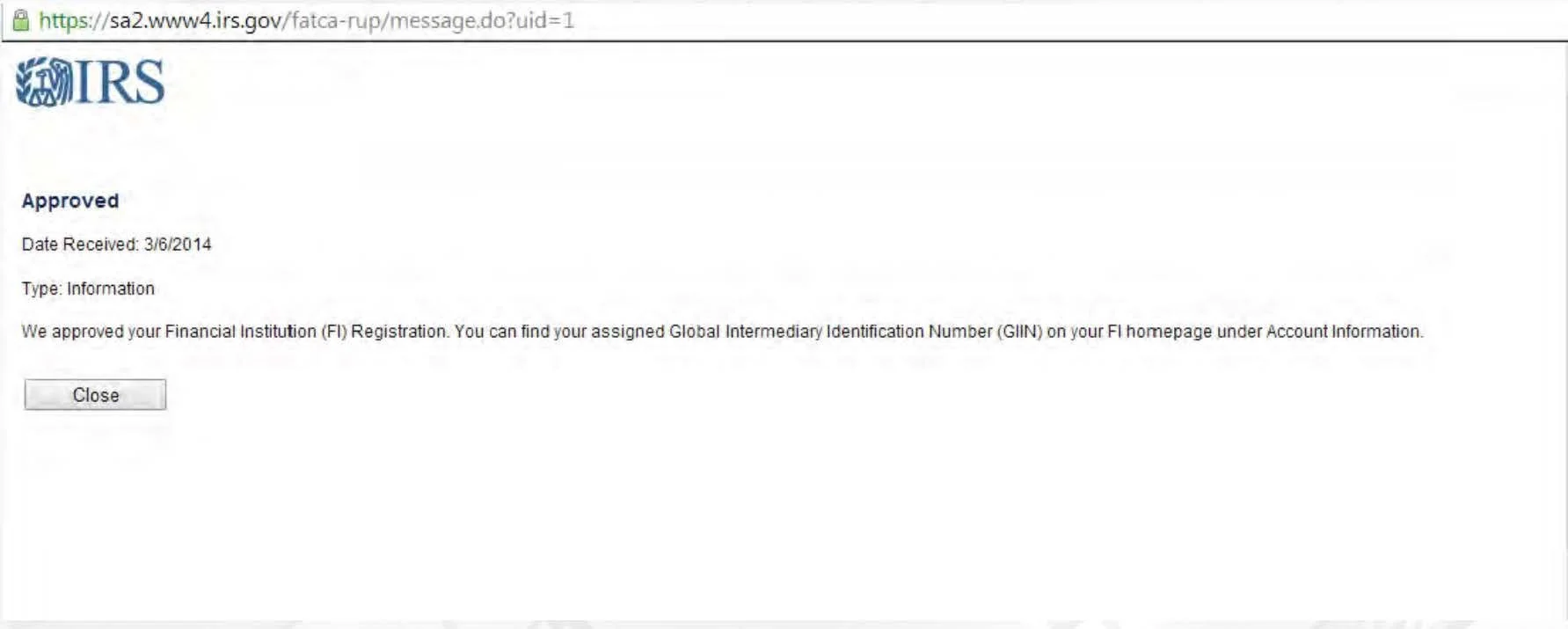

Global Intermediary Identification Number (GIIN): This is a number that will be assigned to an FFI to establish its status for withholding purposes and to identify the institution to the IRS reporting purposes.

IRS FF List: The IRS expected to publish the first list of participating FFIs and registered deemed compliant FFIs on December 2, 2013 and the IRS intends to update the list monthly. FFIs have to register by October 25, 2013 to ensure inclusion on the first list. [These are old dates, the new dates are registration by April 25, 2014 and the first list by June 2014…Maybe]

Relationship Manager: Is an officer or other employee of an FFI who is assigned responsibility for specific account holders on an on-going basis (including an officer or employee that is a member of an FFI’s private banking department), advises account holders regarding their banking investment, trust, fiduciary, estate planning, or philanthropic needs, and recommends, makes referrals to, or arranges for the provision of financial products, services, or other assistance by internal or external providers to meet those needs. Notwithstanding the previous sentence, a person is only a relationship manager with respect to an account that has a balance or value of more than $1,000,000, taking into account the aggregation rules.

Why is FATCA Controversial?

Cost. Although numbers are still somewhat speculative, estimates of the additional revenue raised seemed to be heavily outweighed by the cost of implementing legislation. The Association of Certified Financial Crime Specialists (ACFCS) claims FATCA is expected to raise revenues of approximately US$800 million per year for the US Treasury; however the cost of implementation are more difficult to estimate, and estimates between hundreds of millions and over US$10 billion have been published. ACFCS also claims it is extremely likely that the cost of implementing FATCA (which will be borne by the foreign financial institutions) will far outweigh the revenues raised by the US Treasury, even excluding the additional costs to the US Internal Revenue Service for the staffing and resources needed to process the data produced. Unusually, FATCA was not subject to a cost/benefit analysis by the Committee on Ways and Means.

Capital flight. The primary mechanism for enforcing the compliance of foreign financial institutions is a punitive withholding levy on US assets. This may create a strong incentive for foreign financial institutions to divest (or not invest) in US assets, resulting in capital flight.

Foreign relations. Forcing foreign financial institutions and foreign governments to collect data on US citizens at their own expense and transmit it to the IRS has been called divisive. Canada’s Finance Minister, Jim Flaherty, has raised an issue with this “far reaching and extraterritorial implications” which would require Canadian banks to become extensions of the IRS and would jeopardize Canadians’ privacy rights. There are also reports of many foreign banks refusing to open accounts. forAmericans, making it harder for Americans to live and work abroad.

Extraterritoriality. The legislation enables US authorities to impose regulatory costs, and potentially penalties, on foreign financial institutions who otherwise have few, if any, dealings within the United States. [36] The US has sought to ameliorate that criticism by offering reciprocity to potential countries who sign Intergovernmental Agreements, but the idea of the US Government providing information on its citizens to foreign governments has also proved controversial. The law’s interference in the relationship between individual Americans or dual nations and non-American banks led Georges Ugeux to term it “bullying and selfish”.

Citizenship renunciations. Time magazine has reported a sevenfold increase in Americans renouncing US citizenship between 2008 and 2011, and has attributed this at least in part to FATCA. [39] According to The New American a record number of Americans have given up US citizenship in 2012 “amid IRS Abuse” and “facing an increasingly out-of-control federal government in Washington DC”. [40] According to the BBC, the act is one of the reasons for a surge of Americans renouncing their citizenship – a rise from 189 people in the second quarter of 2012 to 1,131 people in Q2/2013. [41] Another surge in renunciations in 2013 to record levels has been reported in the news media, with FATCA cited as a factor in the decision of many of the renunciants.

American citizens living abroad. According t the Canadian Broadcasting Corporation many Americans abroad may face large fines as a result of this legislation. According to the story, a forty-year-old developmentally disabled man, and a Canadian man married to an American will become some of the victims of this law. According to Time (magazine), American citizens living abroad are unable to open foreign bank accounts in many banks. Effect on “accidental Americans”. The reporting requirements, including penalties, apply to all US citizens, including those who are unaware that they have US citizenship. Since the US considers all persons born in the US, and most foreign-born persons with American parents, to be citizens, FATCA affects a large number of foreign residents who are unaware that the US considers them citizens.

American Taxpayers

From the 2011 tax return, the form 8938 needs to be completed with your US tax return. [For taxpayers living abroad: Joint return $400K in specified foreign assets or more than $600K during the year; other than joint return; $200K in assets or more than $300K during the year.

Swiss Banks will be reporting to the IRS account information for US persons – US-Swiss IGA signed 13-2-2013: Staring for the year 2014, first reports probably sent in 2015.

Savings & Investment Accounts will be reported.

2nd & 3rd Pillar Accounts will likely not be reported.

Your Swiss Financial Institution will ask you (if they have not already) for a W-9 to confirm your US Social Security Number and for your permission to send info to the IRS.

If you have not reported your accounts on the FBAR & 8938 and/or have not reported the income on a US tax return, you should talk with a US tax/legal professional before the IRS receives your information.

Some [local FFI] Swiss Financial Institutions will not be allowed to discriminate against US persons living in Switzerland.

Summary for Foreign Information on “Common” US Tax Forms

Form 3520 – Annual Report to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts, due on the date that the taxpayer’s individual income tax return is due (generally April 15), including extensions;

Form 3520-A – Annual Information Return of Foreign Trust with a US Owner, generally due March 15;

Form 5471 – Information Return of US Persons with Respect to Certain Foreign Corporations, attached to and filed with the taxpayer’s income tax return;

Form 8621 – Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund, attached to and filed with the taxpayer’s income tax return;

Form 8865 – Return of US Persons with Respect to Certain Foreign Partnerships, attached to and filed with the taxpayer’s income tax return;

Form 926 – Return by a US Transferor of Property to a Foreign Corporation, filed with the taxpayer’s income return;

Form 8621 – Must be filed for each PFIC held each year;

Form 8832 – Entity Classification Election, often filed for a foreign company to elect disregarded entity status; thus, the tax responsibility flows through to the owner so that there is no tax at the company level;

Form 8858 – Information Return of US Persons with Respect to Foreign Disregarded Entities, filed with the taxpayer’s income tax return;

Form 8891 – Information Return of US Persons for Beneficiaries of Certain Canadian Registered Retirement Plans

Form 8938 – New form to be included with tax return for individuals with foreign assets over $50,000

Form TD F 90-22.1 NEW FINCEN 114 – Report of Foreign Bank and Financial Accounts, filed by June 30 of each year when, in the previous year, the taxpayer had a foreign bank or financial account worth over $10,000 (for a discussion of recent changes to this form please see “IRS Releases Foreign Bank Account Reporting Form”);

Form 2555 – Foreign Earned Income, generally due April 15 for US citizens and resident aliens living abroad to exclude a certain amount of foreign earnings from taxes and/or to claim the housing exclusion.

Swiss FFIs

Introduction of 30% withholding tax on US source income

FFI (subject to withholding) can avoid withholding by concluding a contract with the IRS

Registration with the IRS necessary, conclusion of a contract for some Swiss FFIs

Swiss FFIs must identify accounts of US persons and must periodically report to the IRS

FFIs not complying with FATCA (non-participating FFIs) risk losing access to US markets and run risks in transacting business with complaint FFIs.

Swiss Financial Institutions

Depositary Institutions

Investment Holding Institutions

Investment Companies

Specified Insurance Companies

(Article 2 – Definitions) Item 7 – Pages 3 and 4 of US-Swiss IGA

Items 9-13 of the IGA cover:

Custodial Institution: Any entity that holds financial assets in account for others and whose gross income from servicing these accounts is over 20% of total gross revenue

Depository Institution: Any institution that accepts deposits in ordinary course of banking or similar business

Investment Entity: Any entity the conducts business in trading (e.g. derivatives, forex, commodity, transferable securities, etc)

Specified Insurance Company: Any insurance company that issues or is obligated to make payments with respect to a cash value insurance contract or annuity contract

Swiss Financial Institution (excludes branches outside of Switzerland or branches or head offices in Switzerland not organized under Swiss law)

Agreement Models 1 & 2 / US-Swiss IGA

Model 1 – Automatic information exchange between domestic tax authorities and the IRS (most reciprocal, some non-reciprocal)

Model 1 – Canada, Mexico, UK, France, Germany, Spain, Cayman Islands, Netherlands, Malta, Jersey, Ireland, etc.

Model 2 – Exchange of information between FFIs and IRS

Model 2 – Switzerland, Japan, Chile, and Bermuda

All IGAs: http://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA.aspx

Swiss Financial Institutions

US / Swiss IGA

Agreed Feb 14, 2013 (Valentine’s Day)

Full text here: http://www.treasury.gov/resource-center/tax-policy/treaties/Documents/FATCA-Agreement-Switzerland-2-142013.pdf

Authorization Clause: Granting of authorization according to article 271 paragraph 1 Stgb (Illegal acts for a foreign state) by Switzerland to domestic financial institutions

Implementation instructions for Swiss FIs

Information Exchange – Administrative assistance by Switzerland based on double taxation agreement (not yet ratified in the US) for group requests regarding uncooperative customers – information exchange

FFI reports data based on approval and declaration of account holders

Report number of account holders and total assets from non-cooperative account holders

Swiss FI not obliged to report non-cooperative US customers to the IRS but have the duty to report to the Estv

Swiss FI must deduct 30% of all taxable revenues from non cooperative US customers (as withholding agents of the IRS) and pay to IRS or terminate customer relations with non-cooperative customers

Swiss FIs must establish processes for identification and monitoring of US taxpayers

Due to Swiss-US IGA certain FIs with many local or regional (EU) activities are considered local FFIs and compliant with FATCA

Independent Asset Managers are subject to registration with the IRS but are exempt from concluding a contract with the IRS

Local FFI and IAM are required to register with the IRS

Duty to report?

Property Insurance, Social Insurance, and Pensions are exempt from FATCA reporting

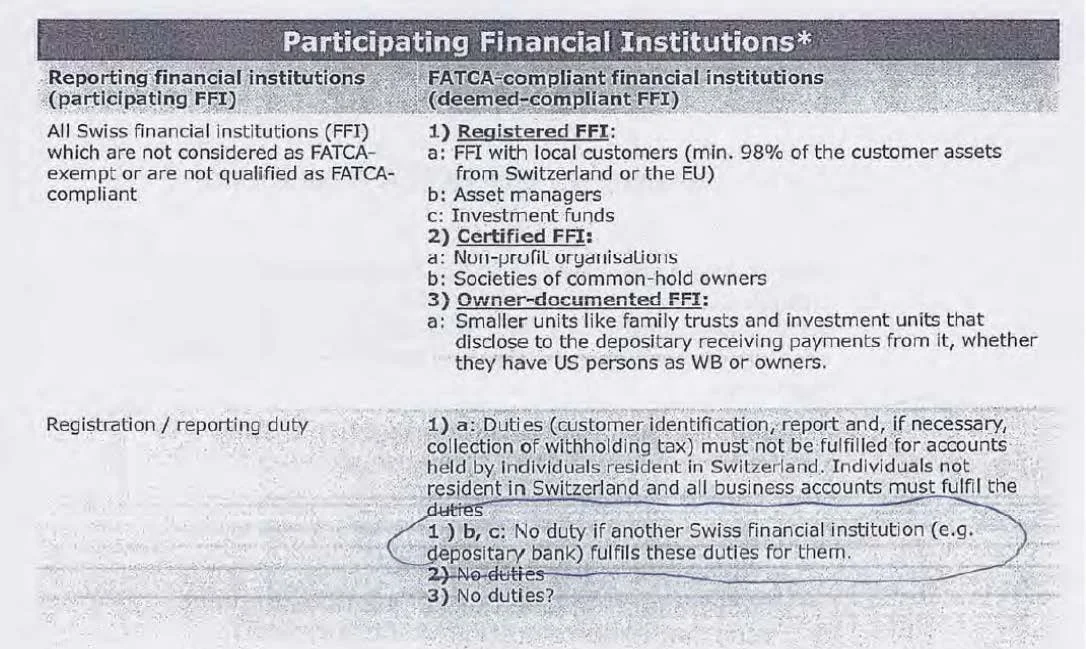

Swiss Independent Asset Managers

Most Likely – Registered deemed compliant FFI

Duty to register

No reporting to the IRS (we think) and not necessary to conclude a contract with the IRS or to withhold taxes from US clients

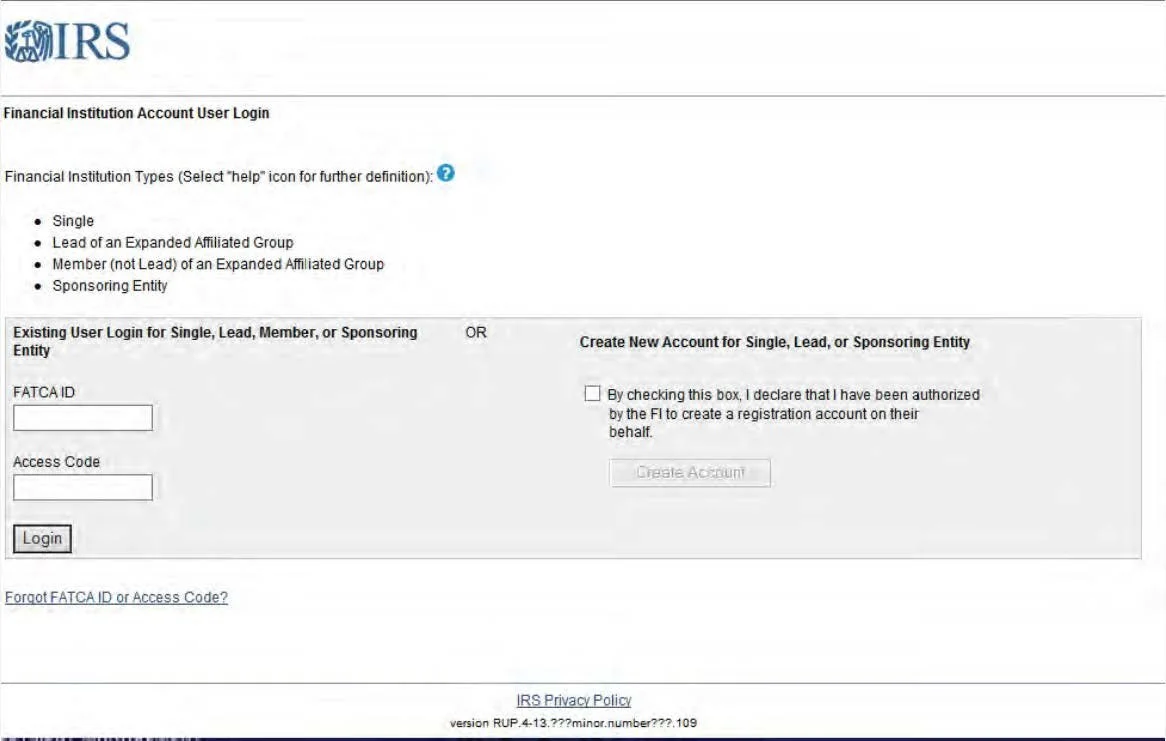

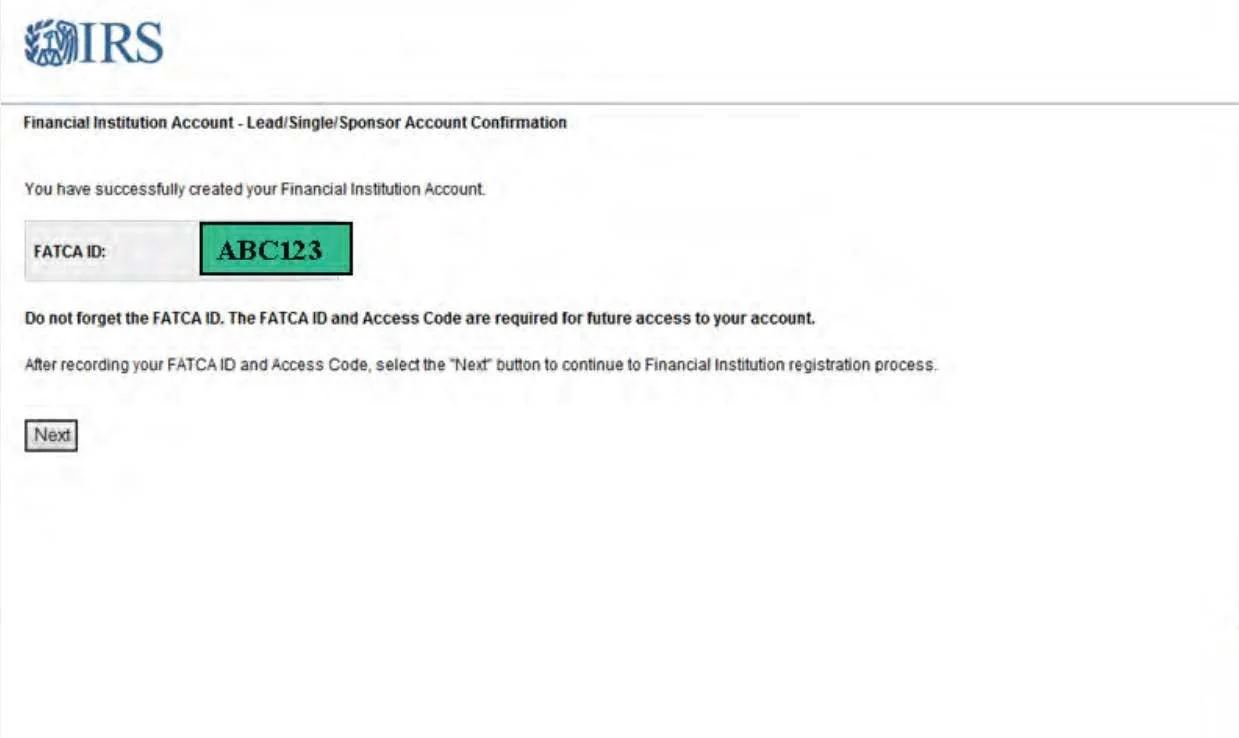

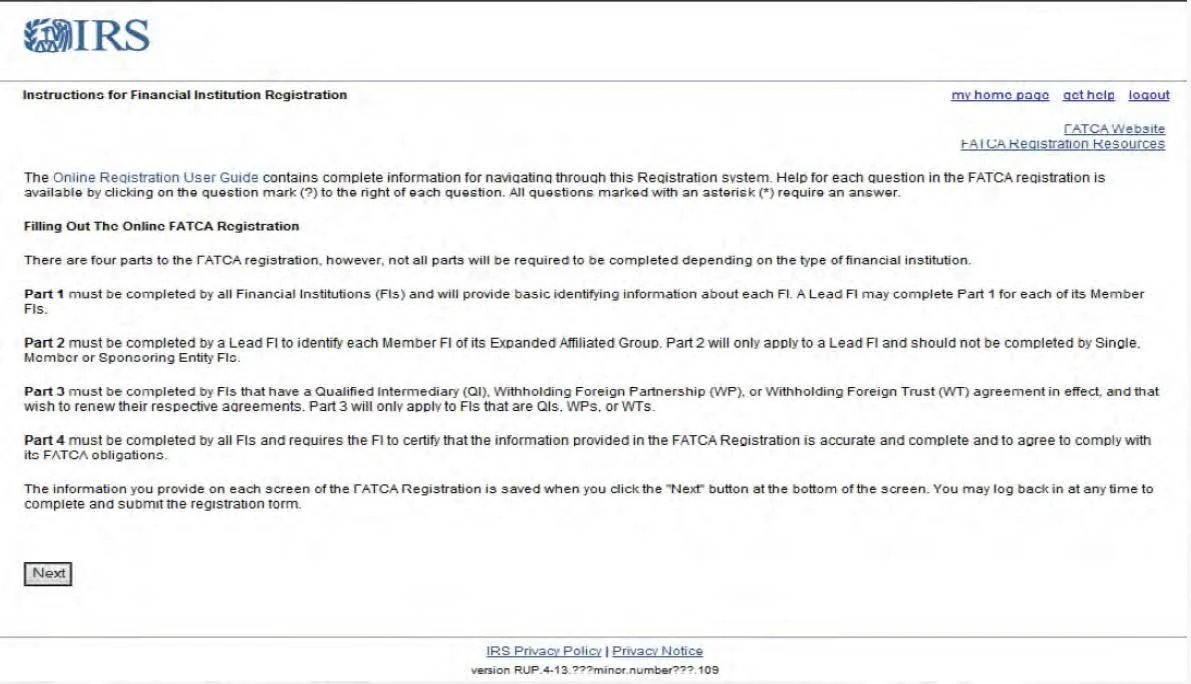

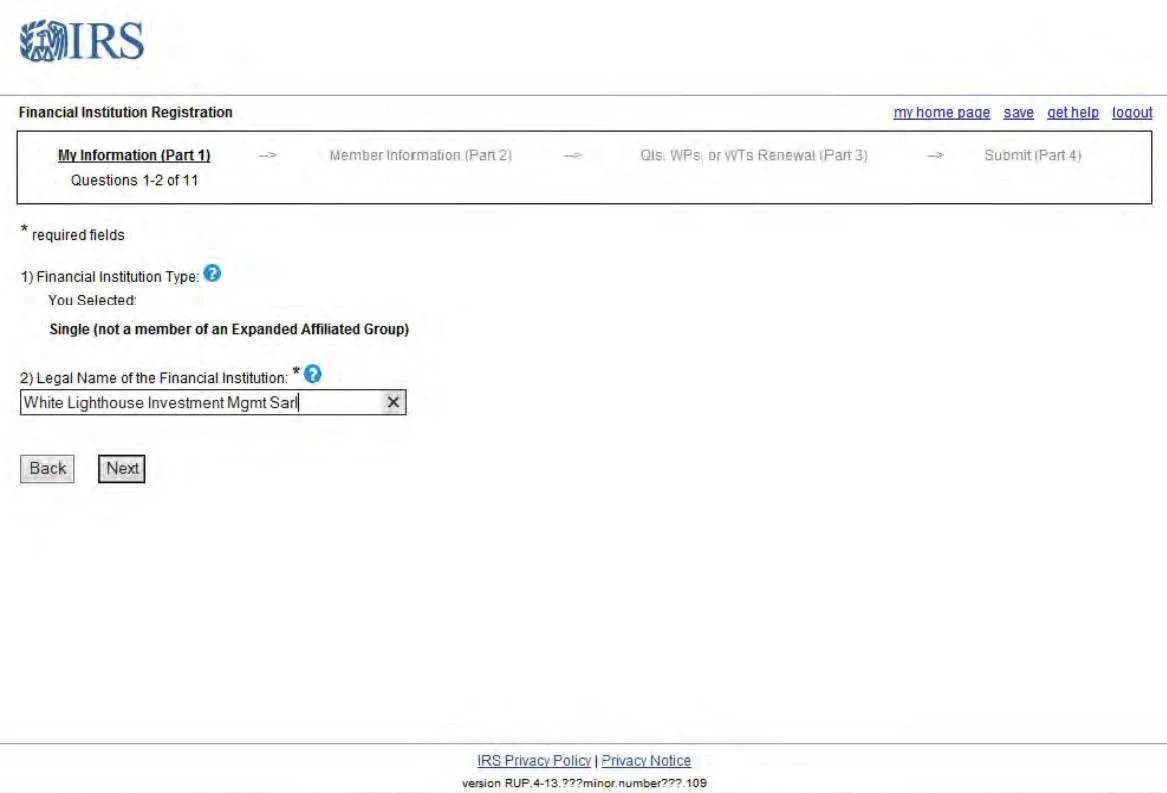

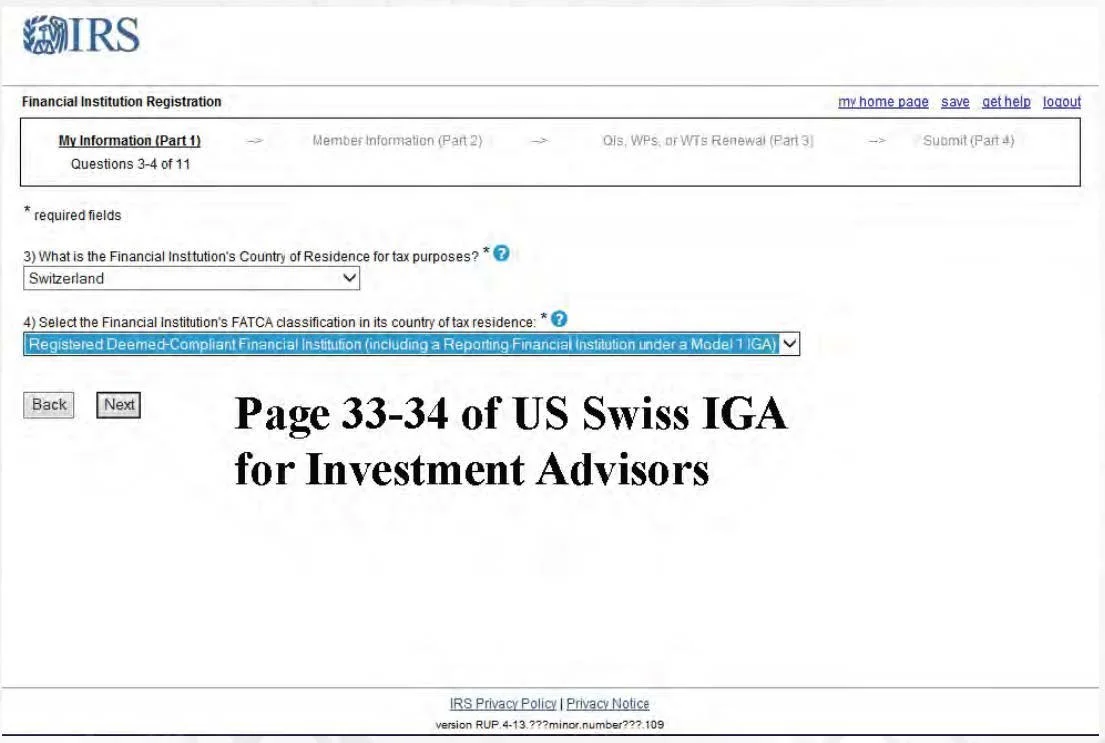

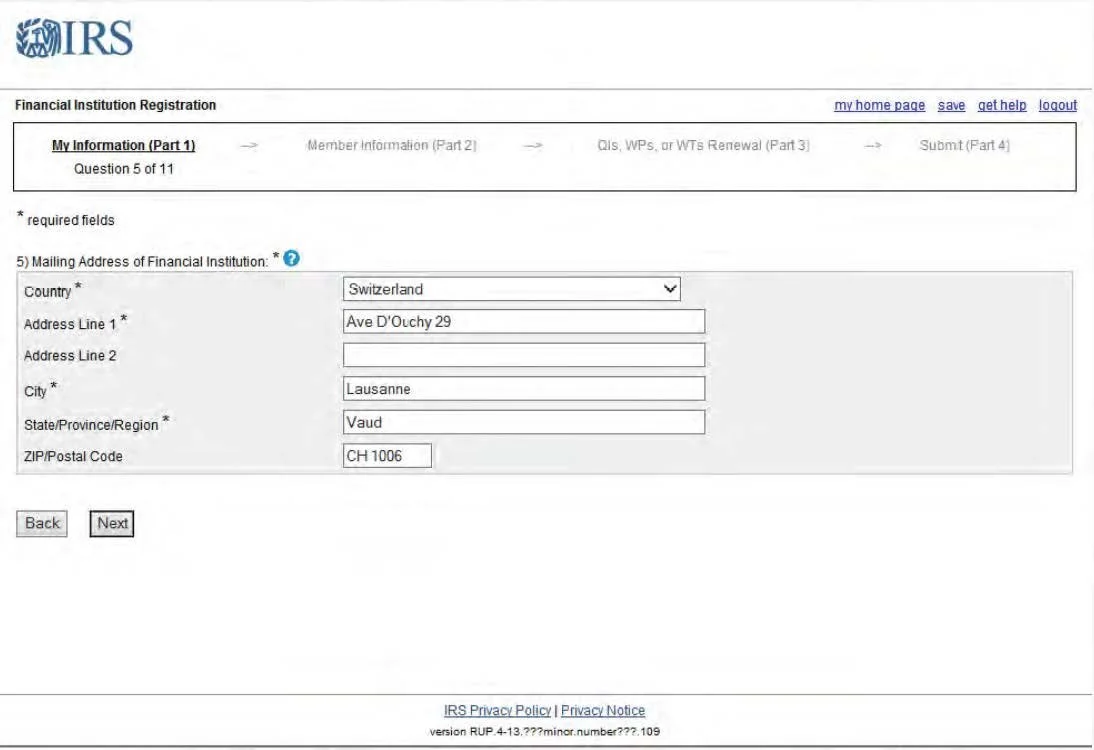

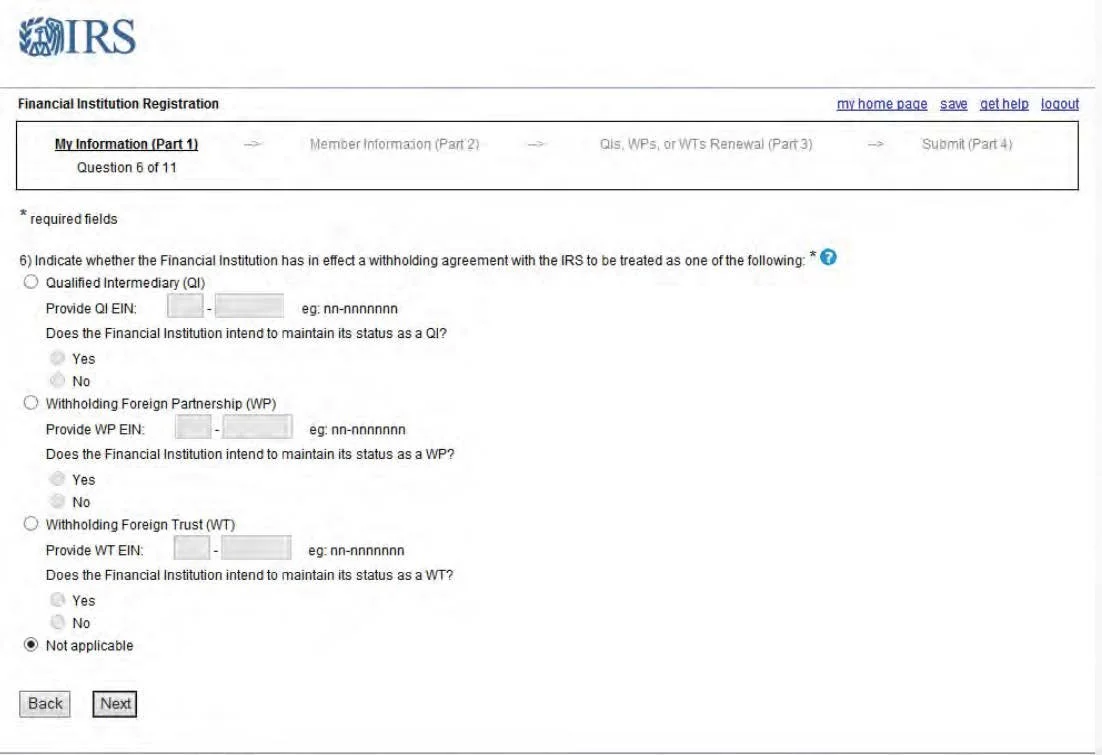

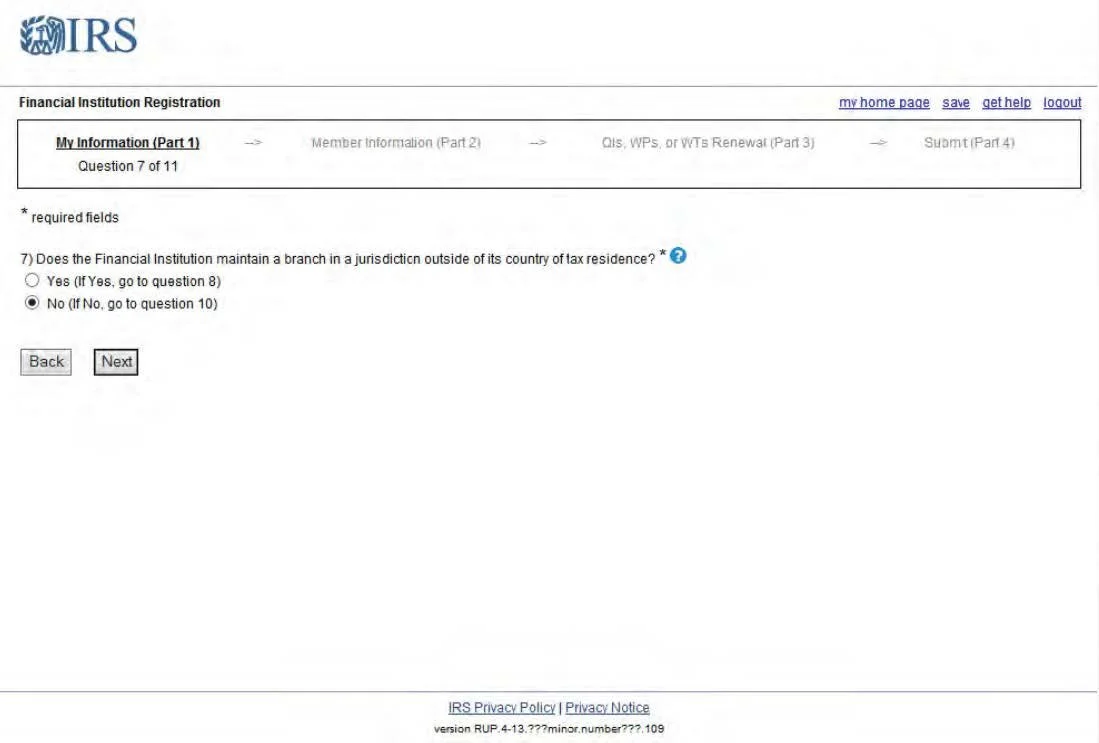

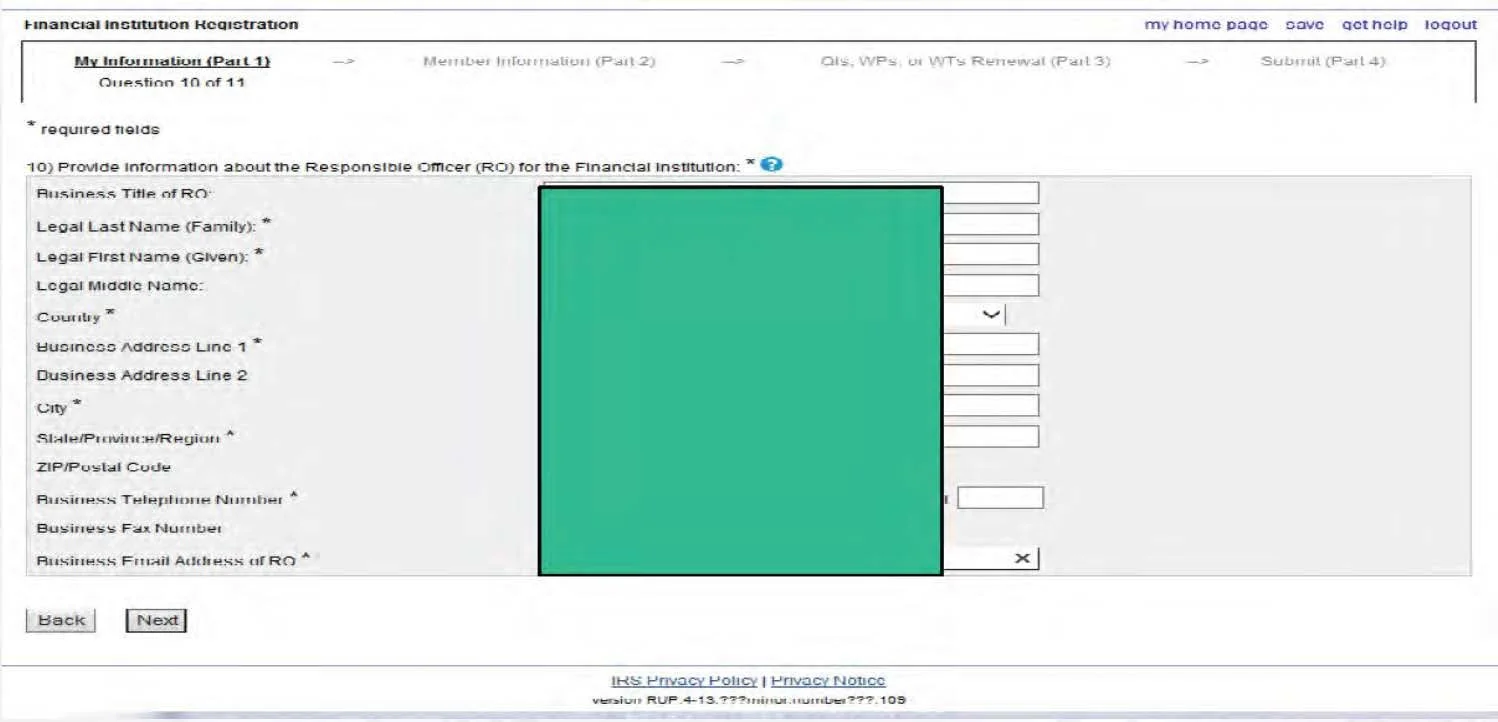

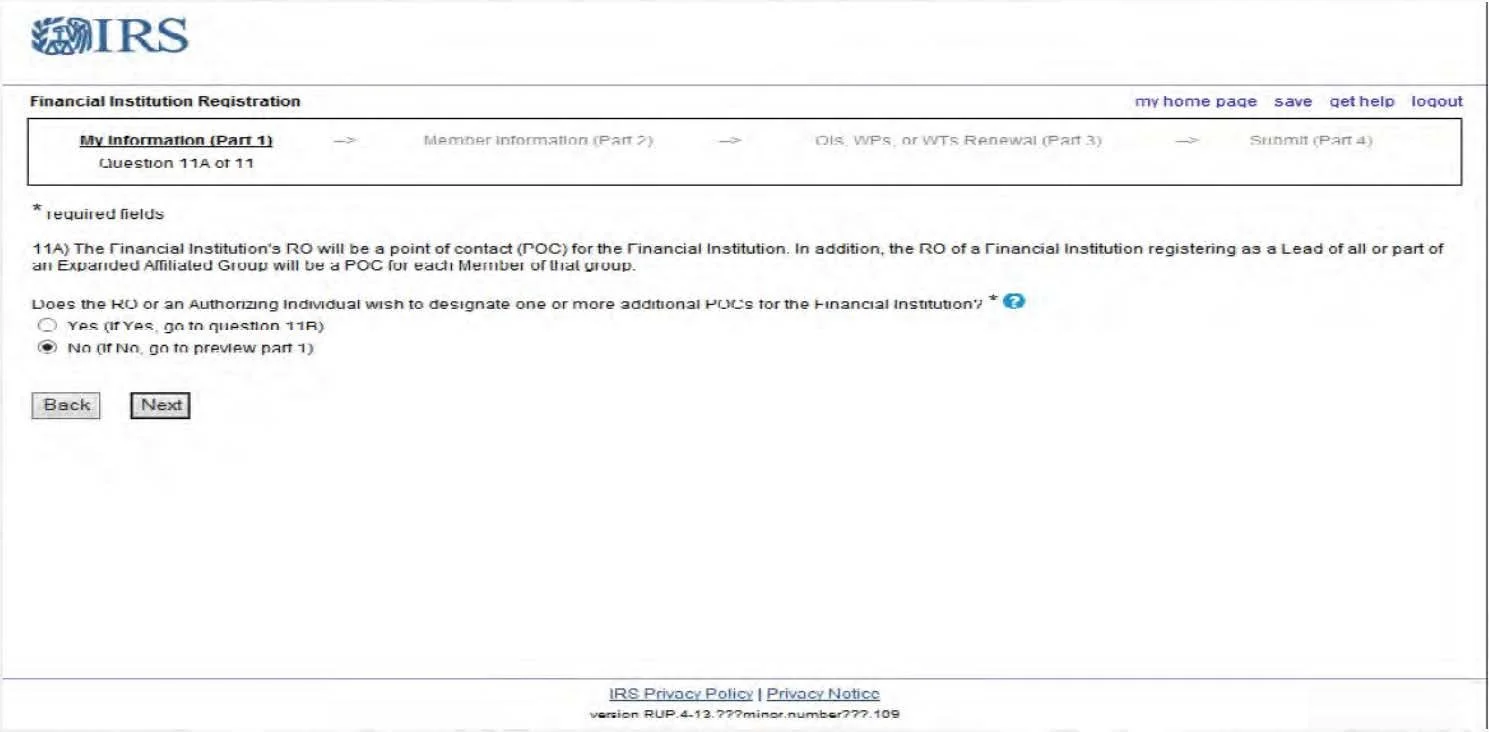

Register at this link: https://sa2.www4.irs.gov/fatca-rup/

Owner documented FFI (e.g. trusts)

No special provisions in IGA

Consider hiring an expert

One or more participating FFIs must vouch for compliance with FATCA duties and accept risks

Participating FFI – Probably not for most IAMs

Full registration with the IRS and conclusion of a contract and reporting responsibilities

Very complex, you will need professional help

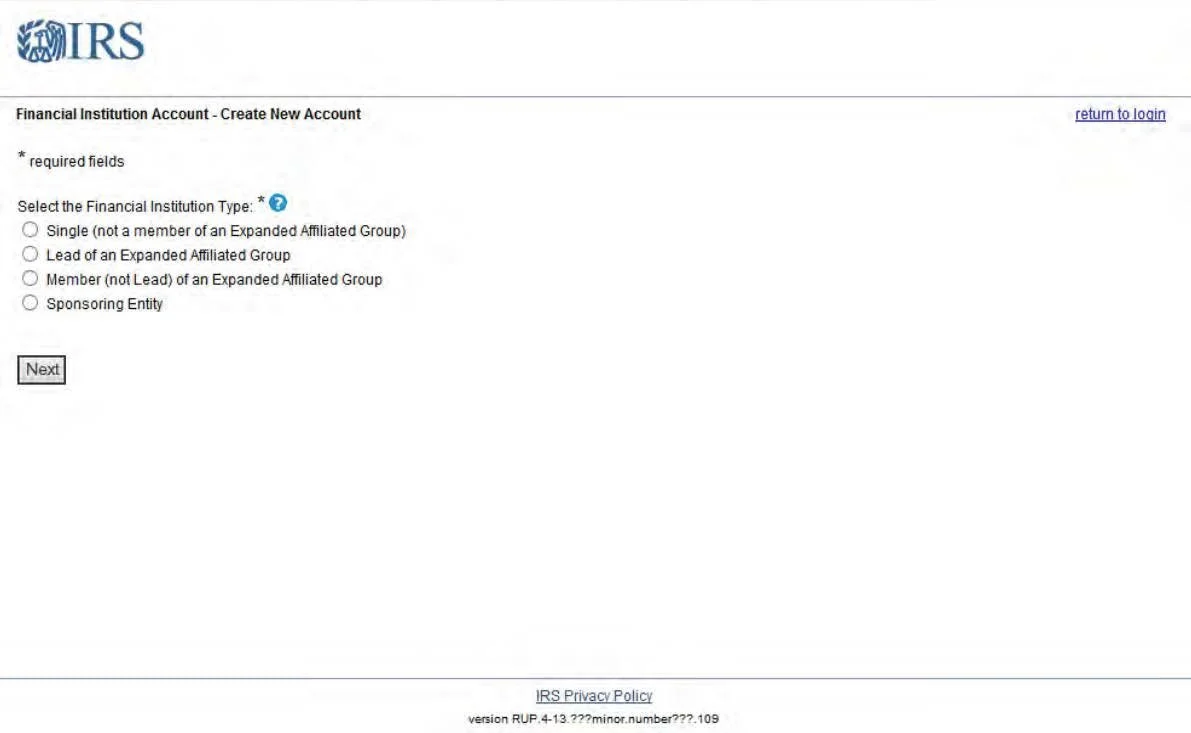

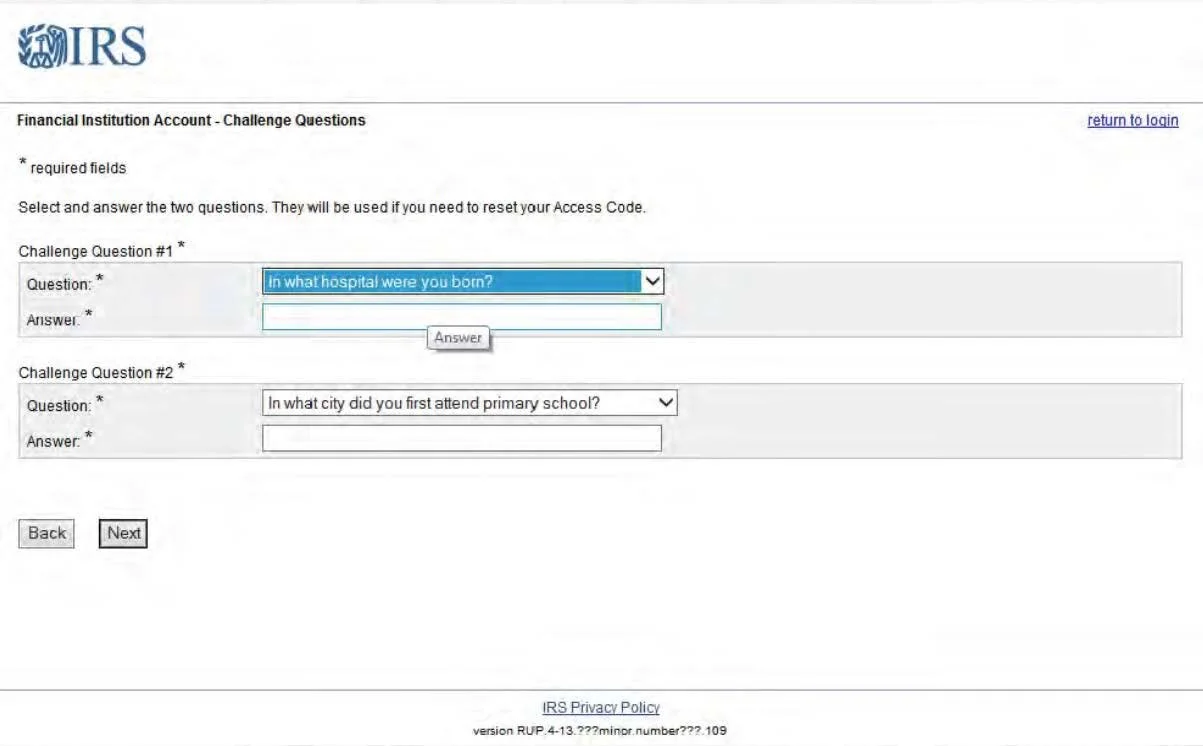

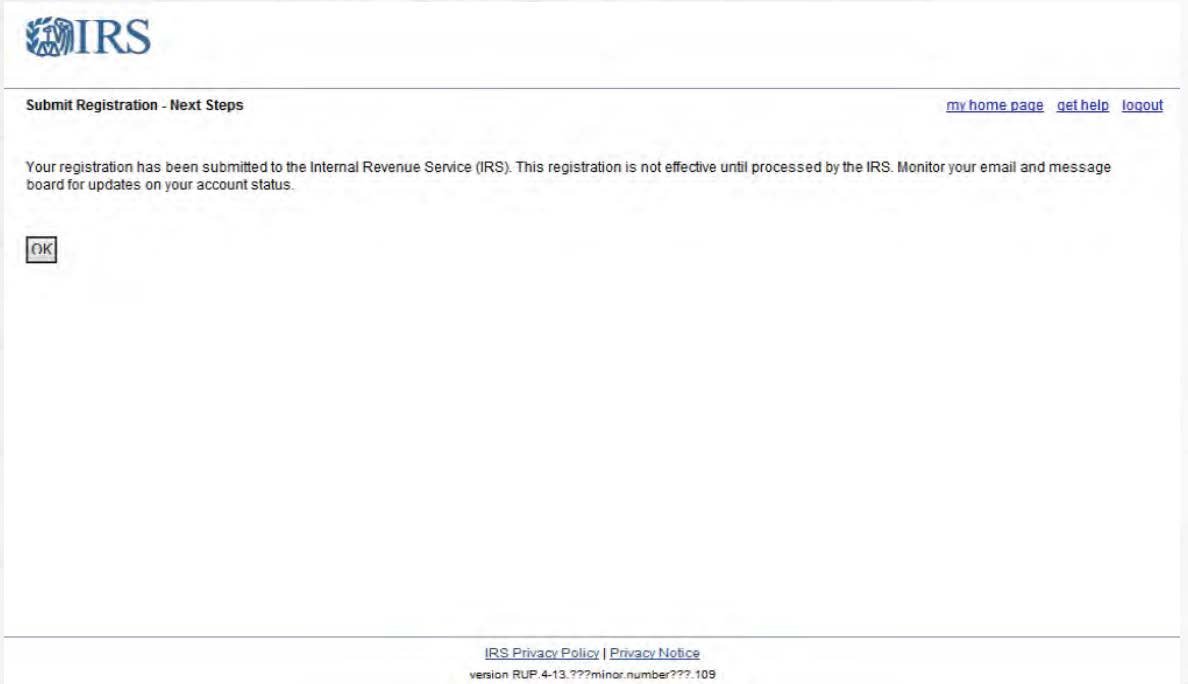

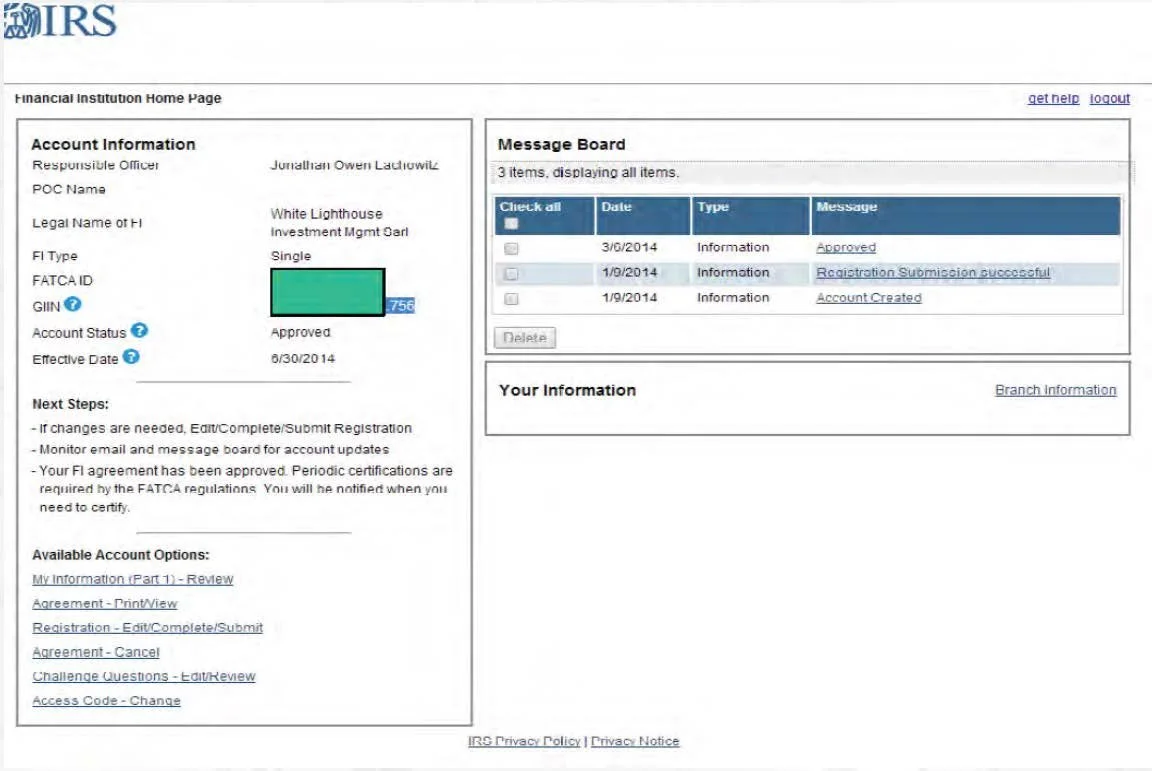

Registering a Swiss IAM – IRS Portal

The following show typical and actual registration process for Swiss IAM

FATCA Timeline

2010 March 18 – FATCA passed into legislation

2010-2012 – Several notices, draft rules and draft documents

2011 – Tax year first US persons filing requirements 8938

2013 – “Finalized” FATCA regulations issued (until the next update)

2013 January – Effective date of most FATCA legislation

2014 January – IRS portal opens (later than expected)

2014 April 25 – Last day for FFIs to register to appear on first FFI list expected for June 2, 2014

2014 June 30 – Effective date, if signed, of FFI agreements

2014 July 1 – FATCA withholding begins & new account procedures

2015 March 15 – First withholding payments made (to IRS) for 2014 tax year

2015 March 31 – First recalcitrant account reporting

Deloitte website provides excellent timeline: http://www.deloitte.com/view/en_US/us/Services/tax/930c9948e681a210VgnVCM100000ba42f00aR CRD.htm

Consultants – FATCA

Full employment

Attorneys

Tax Professionals

Consultants

Advisors

Consultants

The United States graduates approximately 3x as many law students than the economy needs:

http://www.deloitte.com/view/en_US/us/Services/930c9948e681a210VgnVCM100000ba42f00aRCRD.htm

http://www.pwc.com/us/en/financial-services/what-is-fatca.html

http://www.ey.com/GL/en/Industries/Financial-Services/Banking--Capital-Markets/FATCA--resources

https://www.kpmg.com/global/en/industry/financial-services/pages/foreign-account-tax-compliance-actfatca.aspx

http://www.bakermckenzie.com/Switzerland/Zurich

Future of FATCA

Still lots of unknowns from US government

Government data exchange is accelerating and will forever change privacy (not just in terms of tax compliance)

FATCA will go ahead in the short-term

IRS remains underfunded

Other governments will adopt similar regulations (will US cooperate) I think as little as possible; I can not imagine all US financial institutions reporting this type of info to foreign governments (maybe to the IRS though)?

There will be legal challenges (Canada perhaps a good starting point)

Rand Paul (Libertarian) is very early front runner as US Republican Nominee

Links/Sources

IRS Registration : https://sa2.www4.irs.gov/fatca-rup/

IRS FATCA FAQs : http://www.irs.gov/Businesses/Corporations/FATCAFAQs

Wikipedia : http://en.wikipedia.org/wiki/Foreign_Account_Tax_Compliance_Act

US – Swiss FATCA website : http://www.us-person.ch/en/Home/Default.htm

US & Swiss FATCA agreement : - http://www.treasury.gov/resource-center/tax-policy/treaties/Documents/FATCA-Agreement-Switzerland-2-14-2013.pdf

All FATCA IGAs :http://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA.aspx

FATCA Comment Letters : http://bsmlegal.com/fatca-comments.asp

Interesting FATCA Legal Analysis from Canada:http://papers.ssrn.com/so13/papers.cfm?abstract_id=2407264

Article I wrote for L’Agefi(English and French versions available):http://www.white-lighthouse.com/forms.htm

Notes from Presenter

FATCA Legislation is complicated

Various sources used to compile presentation; double-check sources before relying on advice here for your own situtation

Gratefully acknowledge assistance and web presentations from other authors (links in presentation)