To view this presentation in PDF format, click here.

ACA Town Hall Evening | Geneva

May 7, 2014

Jonathan Lachowitz

Financial Planner - Investment Advisor

This presentation is not meant as legal, tax or financial advice to any individual. You are strongly recommended to seek the advice of a professional who understands your specific circumstances before relying on any of the information in this presentation. There may be mistakes and regulations may change or not apply in some circumstances. The presentation may be circulated but should be appropriately cited if used in a professional setting.

IRS Circular 230 Disclosure: Any tax advice in this communication is not intended or written by the author to be used, and cannot be used, by a client or any other person or entity for the purpose of avoiding penalties that may be imposed on any taxpayer.

Introduction

Jonathan Lachowitz

Board Member ACA

Financial Planner & Investment Advisor

Certified Financial Planner ™ -US & CH

Founder of White Lighthouse Investment Management in Lausanne & Lexington, MA

Agenda & Additional Material

Swiss Banks Request for Information from US Citizens

Top 10 Personal Financial Challenges for Americans in Switzerland and How to Address Them

Retirement Planning for Americans in Switzerland – Should I Stay (In Switzerland) or Should I Go (Back to the US)?

What’s new for taxes in 2014

Back-up Slides

Being a Smart Financial Consumer

Tips for American Expatriates

Money Management - Essentials

American Taxes - Living in Switzerland

Money and Children

Estate Planning

Government & Employer Benefits

Common Financial Questions

Retirement - How Much Do I Need?

Swiss Banks Request to US Taxpayers for Personal Tax Info

FATCA – The “why” the banks are asking

DOJ & Swiss Government Joint Statement: August 29, 2013

Your Choices in Responding

A Brief History

The Foreign Account Tax Compliance Act (FATCA), introduced as part f the HIRE Act and enacted into law by the 111th Congress on March 18, 2010, is designed to compel foreign financial institutions (FFIs) and non-financial foreign entities (NFFEs) to provide information to the US Internal Revenue Service (IRS) about US persons who hold accounts with or interests in FFIs and NFFEs.

FATCA was meant to combat offshore tax evasion and to recoup federal tax revenues.

Under US tax law, US persons are generally required to report and pay taxes on income from all sources regardless of where they live.

The IRS previously instituted a Qualified Intermediary (QI) program under Internal Revenue Code §1441 which required participating foreign institutions to maintain records of the US or foreign status of their account holders and to report income and withhold taxes. One report found that participation in the QI program was too low to have a substantive impacts as an enforcement measure and was prone to abuse: As has been demonstrated by UBS and Credit Suisse as well as the relatively small number of Overseas Americans filing tax returns and FBARs.

FATCA in 1 Minute – For Individuals

From the 2011 tax return, the form 8938 needs to be completed with your US tax return. For taxpayers living abroad:

Joint return – $400K in specified foreign assets or more than $600K during the year

Other than joint return – $200K in assets or more than $300K during the year

Swiss Banks will be reporting to the IRS account information for US persons – US-Swiss IGA signed 13-2-2013: Starting for the year 2014, first reports probably sent in 2015

Savings & investment accounts will be reported

2nd and 3rd Pillar accounts should not be reported

Your Swiss financial institution will ask you (if they have not already) for a W9 to confirm your US Social Security Number and for your permission to send info to the IRS

If you have not reported your accounts on FBAR & 8938 and/or have not reported the income on a US tax return, you should talk with a US tax/legal professional before the IRS receives your information

Some [local FFI} Swiss Financial Institutions will not be allowed to discriminate against US persons living in Switzerland

DOJ & Swiss Government Joint Statement: August 29, 2013

DOJ announces program to encourage Swiss banks to cooperate in DOJ investigation of offshore tax evasion

Swiss government encourages all Swiss banks to participate in the program

Available to banks not currently under criminal investigation:

Agree to pay substantial penalties

Make a complete disclosure of their cross-border activities

Provide detailed information on an account-by-account basis for accounts in which US taxpayers have a direct or indirect interest

Cooperate in treaty requests for account information

Provide detailed information as to other banks that transferred funds into secret accounts or that accepted funds when secret accounts were closed

Agree to close accounts of account holders who fail to come into compliance with US reporting obligations

Banks meeting criteria exchange information & money for non-prosecution (category 2) or non-target letters

Link to full text of statement: : http://www.justice.gov/opa/pr/2013/August/13-tax-975.html

Link to program: : http://www.justice.gov/iso/opa/resources/7532013829164644664074.pdf

Banks will pay a penalty of between 0% and 50% of the US tax payers maximum account value

Banks want your help in getting them to 0% that is why they are asking for information

Banks are generally asking for FBARs, an attestation from the client, and tax advisor that the accounts and income have been properly reported to the IRS and Department of Treasury

Banks are also asking for clients to give up certain Swiss rights with respect to the handling of their private information

In some cases, banks are asking for copies of tax returns

In some cases, banks are blocking access to client funds

What to give your banks or former banks?

| Do you want to keep your banking relationship? | |||

|---|---|---|---|

| YES | NO | ||

| Are you US tax compliant? |

YES | - Give info requested - Redact info not related to that bank - Consider not giving up Swiss Privacy rights |

- Give info requested if you want to be nice; redact info not related to that bank - No obligation especially if you have no money left there - Your name may end up on a "list" so keep good records |

| NO | - Get compliant and likely with a professional - Then see box above |

- Get compliant and likely with a professional - Your info may be handed over and this may get you in trouble |

|

In most cases, it is reasonably likely that your information could be sent to the US government, but it may take awhile.

Swiss Banks Request to US Taxpayers for Personal Tax Info

More information available

Full article: : http://americansabroad.org/files/6013/8618/6297/swiss-banks-versusus-citizens.pdf

Abridged version, Ellen Wallace at Geneva lunch: http://genevalunch.com/2013/12/03/banks-ending-year-with-letters-to-us-clientsupdate/

Top 10 Personal Financial Challenges for Americans in Switzerland and How to Address Them

1 – US Tax Compliance – Keep up with ever more complex rules

File your tax returns including worldwide income, pay your taxes on time and file your FBAR/FinCEN 114 and you will avoid 90% of “problems” that overseas Americans run into

Net page has some of the most common overseas tax forms

Employer and employee contributions to retirement accounts are taxable in the US (flaw in the treaty) – Track your US tax basis

Owning non-US investment funds is for most US taxpayers a recipe for trouble, especially without a tax advisor and even in 3rd Pillar accounts

Even the most “simple” situation can be challenging to report properly

2 – US Tax Planning – Using the rules in your favor

If you have earned income and it is not all excluded, you can make a tax deductible IRA contribution

Having a year with no income or low income for the US, consider a Roth conversion of US retirement accounts

Watch how your investments are structured: ETFs are often better than similar Mutual Funds due to less capital gains distributions

Consider gifting and/or titling of accounts especially if married to a non-citizen spouse

3 – Saving for Retirement

By far the most important thing is to save, regularly, this will have the biggest impact on your retirement

Don’t “save” on Swiss taxes only to increase your US taxes

TRACK YOUR US TAX BASIS in your 2nd and 3rd Pillars to help avoid double taxation in retirement

Retirement savings in a non-tax-deferred account has other tax and non-tax advantages; Capital gains treatment is better, diversification, and personalization of strategy is possible

Whether in Switzerland or the US, you will probably live longer than you think (on average); and Switzerland still has a mandatory retirement age for most jobs; You may need to be saving more than you think

Understanding of how US Social Security and Swiss AVS rules can work for or against you, especially with the deferral of benefits

4 – Estate Planning

Your US Will may not be executed the way you are expecting if you die in Switzerland

If you are not Swiss you can elect to have your home country law apply

A Swiss notary or attorney can help you get your paperwork in order

Switzerland has forced heirship rules, which means your children will inherit some of the estate upon the death of the first parent…Unless you choose items 2 and 3 above.

5 – Insurance – Especially for life insurance

Life insurance is most valuable in the currency it would be needed

US taxpayers should try to avoid building cash values or investing in non-US compliant life insurance

Consider having a spouse own the policy for US estate planning purposes

Medical insurance is private in retirement in Switzerland; Medicare with supplemental insurance can be a reasonable alternative, but not available outside the US

Term insurance is generally far cheaper in the US but most US companies cannot sell insurance to Swiss residents

6 – Investment Management Services

Difficult (not impossible) to find comprehensive advice for US persons at a reasonable price if Swiss domicile of account is preferred

Strongly consider using a US investment account; prices tend to be far more competitive, you can own most Swiss investments in a US-based account

Being SEC registered does not mean a firm has any particular competence in working with US persons

Do your homework and be clear about what type of advisor you are looking for – Many (in the US and Switzerland) are strictly sales people with a fancy title

7 – Finding Professional & Trustworthy Services – Also at reasonable price

If your bank/banker has asked you to leave because you are a US person, use this as an opportunity to go through a good selection process – Far too many people research a new restaurant more than they do their advisors

Get references and follow through

The community of professional advisors who serve US persons (tax, legal, financial, etc) is small – Sometimes going outside the country can help

Most good advisors don’t need to advertise and don’t need to look for new clients; they can also afford to reject new clients who are not good for their business

8 – Managing Currency Risk

Holding cash in one currency that will need to be spent in another currency is risky (exchange rates)

Holding cash for “long term” investment in the currency it will be spent is risky (inflation)

Global stocks including a large part of the SMI are highly correlated to the US Dollar, not the Swiss Franc

Nestle, Novartis, and Roche – Buying shares in a company that are denominated in Swiss Francs are not much “safer” than holding stocks in dollars or euros

Holding dollars for the last 40 years you saw the dollar go from buying 4 Swiss Francs to buying less than 1 Swiss Franc; holding shares in the S&P saw an annual return, in Swiss Francs of close to 10%

9 – Real Estate

Make sure you understand the income tax implications in the US of your Swiss real estate in terms of: mortgage, interest deduction, the sale of your home (capital gains or losses), and the paying off of your mortgage (capital gains and losses)

This is a big shock to lots of US persons, see your tax advisor for good advice

The main reasons people make money in real estate is leverage and forced savings (to pay down a mortgage) over a long period of time – Luck helps

The main reason people lose money in real estate is leverage, unfortunate timing, and too short a time horizon

10 – Feeling Powerless to “Change the System” to Be More Fair

Join ACA (or better, volunteer for ACA) and encourage your friends to join too - A very small organization with very little funding but lots of passion; has a voice in Washington and in the US press; and it is increasing

Vote in Federal Elections & contact your representatives in Congress

Contact the US Embassy

Talk to the press

Nothing will change in Washington DC without individual citizens working for change

Summary for Foreign Information on “Common” US Tax Forms

Form 3520 – Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts, de on the date that the taxpayer’s individual income tax return is due (generally April 15), including extensions

Form 3520A – Annual Information Return of Foreign Trust with a US Owner, generally due March 15

Form 5471 – Information Return of US Persons with Respect to Certain Foreign Corporations, attached to and filed with the taxpayer’s income tax return

Form 8621 – Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund, attached to and filed with the taxpayer’s income tax return

Form 8865 – Return of US Persons with Respect to Certain Foreign Partnerships, attached to and filed with taxpayer’s income tax return

Form 926 – Return by a US Transferor of Property to a Foreign Corporation, filed with the taxpayer’s income return

Form 8621 – Must be filed for each PFIC held each year

Form 8832 – Entity Classification Election, often filed for a foreign company to elect disregarded entity status; thus, the tax responsibility flows through to the owner so tat there is no tax at the company level

Form 8858 – Information Return of US Persons with Respect to Foreign Disregarded Entities, filed with taxpayer’s income tax return

Form 8891 – Information Return of US Persons for Beneficiaries of Certain Canadian Registered Retirement Plans

Form 8938 – New form to be included with tax return for individuals with foreign assets over $50,000

Form TD F 90-22.1 New FinCEN 114 – Report of Foreign Banks and Financial Accounts, filed by June 30 of each year when, in the previous year, the taxpayer had a foreign bank or financial account with over $10,000 (for a discussion of recent changes to this form please see “IRS Releases Revised Foreign Bank Account Reporting Form”)

Form 2555 – Foreign Earned Income, generally due by April 15 for US citizens and resident aliens living abroad to exclude a certain amount of foreign earnings from taxes and/or to claim the housing exclusion

Retirement Planning for Americans in Switzerland – Should I Stay (In Switzerland) or Should I Go (Back to the US)?

Often a lifestyle not a financial decision

Crossing borders presents threats and opportunities

Cost of living: Matching income to expenses - Currency

Tax system

Health Benefits

Language

What’s New for US Taxes in 2014

Gift and Estate Tax Limits

Tax Summary Pages 1-6

2014 Gift & Estate Limitations

Annual gift exclusion amount increased to $14,000 in 2013 from $13,000; Remains at $14,000 for 2014

Federal Estate Tax (Lifetime Gift Exclusion amount) $5.3 million and indexed annually for inflation

2014 Gift Exclusion amount to non-citizen spouse increases to $145,000 (up from $143K in 2013)

Federal Estate Tax is not scheduled to sunset though the President has already proposed reducing it

2014 Tax Summary – What’s New

FEIE – $99,200 for 2014

Top US federal tax rate 39.6% for income $457,600 and up (married filing jointly, $432K HOH, $406K single)

http://forbes.com/sites/kellyphillipserb/2013/10/31/irs-announces-2014-tax-brackets-standarddeduction-amounts-and-more

US Long Term Capital Gains rate - 20%

Medicare surcharge (Obamacare tax) 3.8% – for joint filers > $250K, for individuals > $200K

Itemized deductions & personal exemptions phase out for individuals earning > $245K and couples earning > $305K

AMT has been “permanently” inflation adjusted

Personal exemption is $3950, but starts to phase out at $350K, completely phased out for income above $427K (both limits for MFJ, less for individuals)

Kiddie Tax – Children can earn $1000 with no taxes, up to $2000 at reduced rate and over $2000 at parents rates

$5500 IRA contribution limit (traditional IRA) $6500 if over 50 years old

Federal gift tax exclusion $14,000

Federal estate tax exclusion (for US persons) $5,340,000 – Only $60,000 for non-US persons holding US situs assets – Federal estate tax rate 40%

Obamacare

Net investment income tax: 3.8% on the lesser of

Your net investment income

The amount of your modified adjusted gross income (basically, your adjusted gross income increased by an amount associated with any foreign earned income exclusion) that exceeds $200,000 ($250,000 if married filing a joint federal income tax return, $125,000 if married filing a separate return)

Effective 2013 tax year and does apply to foreign income

For 2013 tax returns, if you are a high-income wage earner, [over $250 MFJ] with a W-2 [and self-employment income] at the end of the year, you will have a .9% ‘Additional Medicare Tax’ (AdMT) on income over $200K. This will be reported on new IRS Form 8959. [Effective 2013 tax year and does not apply to foreign income] and will not be matched by employers

No mandatory health insurance if you live outside the US

FBAR

FBAR and FinCEN 114 can only be e-filed on the FINANCIAL CRIMES ENFORCEMENT NETWORK

http://bsaefiling.fincen.treas.gov/NoRegFBARFiler.html

The old FBAR form TD F90-22.1 will be replaced by the FInCEN 114. The TD F form had 3 pages of instructions

The FinCEN 114 has 19 pages of instructions

If your tax status is MFJ you must also prepare FinCEN 114 – Both spouses having to sign this form

If your computer does not use a Windows operating system, you cannot access this site

If you use either Firefox or Google Chrome as your browser, you might have difficulty accessing this site

If a ‘third party’ (ie tax preparer) will be e-filing for you, you must present a signed FinCEN 114A to that preparer

Form 8938

Specified foreign financial assets must be reported on this form – There are filing level ‘differentials’ with lower amounts for US domiciled filers and expat filers:

MFJ overseas: $US400,000 balance for all specified foreign financial assets as of 31 Dec 13 or balances on any day during the year that value was $US600,000

MFS or Single overseas: $US200,000 at 31 Dec or $US300,000 as highest aggregate amount during the year

The 2012 Form 8938 was 2 pages – The 2013 version is 3 full pages

There is a 12-page set of instructions, with examples, explaining what is considered a specified foreign financial asset

Passive Foreign Investment Corporations – PFICs – Non US Investment Funds

Form 8621 – For filing by the Shareholder of a Passive Foreign Investment Company or a Qualified Electing Fund

This includes any business investment with under 10% ownership but with a market value of over $US25,000

At the end of 13 pages of instruction for this form, the IRS estimates that it will take a PFIC owners 15 hours, 4 minutes for annual record keeping; 11 hours, 13 minutes for learning about this form; and 20 hours, 21 minutes for form preparation and filing…Just for owning an investment outside with an end of year value of $US25,000.

PFIC taxation

Preferred Method is Market to Market (assume it is sold at the end of each year and report income annually) – No Long Term Gains Treatment

If not Market to Market, other options include getting the funds to report “properly” for the US or possibly paying large taxes and penalties if profitable and held for a long time.

Message: It is not worth owning PFICs for 99% of Americans overseas

Concluding Thoughts

Time and education are your best assets

Are you passionate about what you are doing? If not, what are you doing about it?

Are you saving enough? Save early and often – Time Value of Money is a Miracle

Are your expectations realistic?

Remember Risk vs Reward – There is no such thing as a free lunch

Keep fees and expenses low – But not too low

Find professional help when you need it – Hire people who are more qualified than you: A financial planner can help you stick to your plan!

Understand the real difference between gambling and investing

Don’t expect government, company, family, or children to take care of you: If they do, that’s a bonus – You are in the driver’s seat

Don’t look at your portfolio too often

Things change, be prepared!

Back-Up Slides

Being a Smart Financial Consumer

Investment of your time – even if the subject is not interesting

Together with your spouse or partner

Educate yourself

Hiring a professional where specialists are needed

You will need to pay for most good professional advice

Being a good client – Most good advisors choose you as much as you choose them…Be respectful, honest, and timely

E.g. If you have had 5 new tax advisors in 5 years, the problem may not be the tax advisors

The Swiss expat community is small

Know your costs

Know your rights and obligations

Comparison shopping

Choosing a Financial Advisor

Do you need a financial advisor or planner? Why?

What is a financial advisor? Different titles…

Whose interests do they put first? Are they a fiduciary, employee, or salesperson?

What are you looking for and what do you think you need?

A financial plan?

Investment advice?

Retirement advice?

Get references from people you trust – Ask the one thing your reference does not like

What licenses, education, registrations do they hold? CFA, CFP®, CHFc, or PFS (for CPAs) are some of the most respected.

What experience do they have? Would you be a typical client?

How does the advisor get paid?

Is their advice objective? How do you know? Are they paid more to sell their company’s product?

Will they consider or advise on assets not under their management?

Ask them if they can beat the market?

Have they been involved in any lawsuits, consumer complaints, or other disciplinary action?

Financial Advisor Checklist

Education and Qualifications

Is your advisor a fiduciary – putting your interests first?

How is your advisor paid?

Is your advisor qualified to give comprehensive advice?

Is your advisor a salesperson – Do they advise on products they are not selling?

Is your advisor upfront about “beating the market”?

Will your advisor try to prevent you from making mistakes?

Has the advisor been involved in any lawsuits or consumer complaints?

Full article at this link: 8 Things Your Financial Planner Won’t Tell You http://articles.moneycentral.msn.com/RetirementandWills/CreateaPlan/8ThingsYourFinancialPlannerwontTellYou.aspx

Tough Questions for Your Financial Advisor

What was your largest mistake in the past 10 years? What did you learn from it?

Do your financial incentives always line up with my best interests?

How do you manage conflicts between your goals as an employee and what is best for your clients?

Would you change your strategy for managing my account based on changes in the macro-economy?

Who in your firm actually makes the decisions on my account?

How have your client’s portfolios performed over the past 10 years?

If I wanted to buy a couple of broad based (low cost) index funds or ETFs, which would you recommend?

May I speak with one of your former clients?

If you ask for a referrals is more than one choice presented? And/Or an explanation of why a specific client name is given?

When was your last job change and why?

For US Registered Advisors

Investment Advisor Search: http://www.advisorinfo.sec.gov/IAPD/Content/Search/iapd_Search.aspx

Check out the firm and the individuals

They should offer a copy of their ADV 2 (firm and individual)

To verify CFP® certification –http://www.cfp.net/

Tell me about some of the outside professionals you work with: Do you pay or get paid for referrals? Do you disclose this generally to clients?

Ask about their regulations, auditors (when needed)

Ask about continuing education

Tips for American Expatriates

Get a regular copy of your free annual credit report +1 877 322 8228

Consider implementing a security freeze to prevent ID theft: http://redtape.msnbc.com/2007/11/now-a-way-to-st.html#posts

Get a regular copy of your US Social Security Statement: http://www.ssa.gov/

File your Annual US Tax Returns – It is now being checked upon passport renewal!

Keep a US credit card, with a US address

Keep a US address (for investing, credit cards & possible insurance)

Get a US phone number (Skype, call 800 number for free)

Review life insurance and long-term care insurance in the US

Review a US-based will

Investigate what happens if you were to die while living overseas (Swiss law is different than US)

If you plan to return to the US, work with advisors who are experienced with the US “system” (financial, tax, legal, etc)

Travel to the US only on your US passport

Vote in Presidential elections (Federal OK, Local elections not advised from overseas)

Check out previous residence - “unclaimed property”

If you are married to a non-American, make sure you know the estate planning and gift tax implications – There are advantages and disadvantages

Money Management Essentials

Most important investment advice

Top money management essentials - mistakes

Risk

3 Ways to invest

List to asset classes

Most Important Investment Advice

Diversification

Dollar/CHF Cost Averaging

Time Horizon – Liquidity

Costs

Conflicts of Interest

Risk

Hard to define for most people

Loss of some or all of investment amount

Asset Manager – Uses measures such as standard deviation from “expected return”

Consider: time frame, inflations & your goals

Understand difference between risk and volatility

3 Ways to Manage Money

Market timing

Trying to decide where a market, particular security, or asset class currently is, where it may be going and when

Security selection

Choosing one investment over another

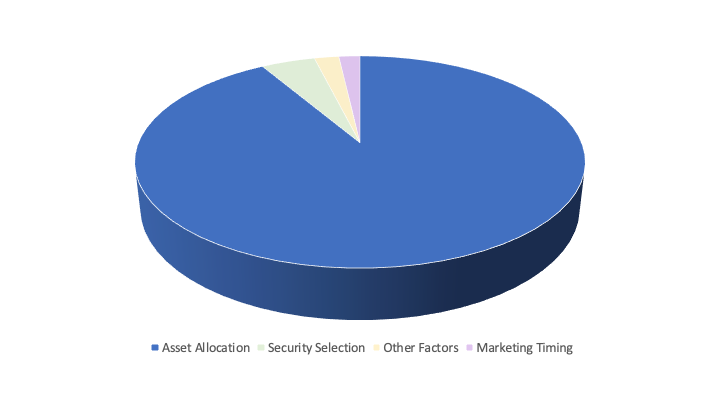

Asset allocation

Spreading the money in your portfolio between different types, or classes, of investments

| TYPE | PROS | CONS |

|---|---|---|

| Asset Allocation | - Investing not speculating - Proven long-term strategy - No guess work or emotions - Focuses on whole portfolio - Easy to manage |

- Boring - Won't get rich quick - Periodic rebalancing needed - Have to decide which classes - Inexperienced investors don't like some classes |

| Security Selection | - Fun and exciting to bet - If you are right a lot more than wrong, get rich quick |

- Too hard, too risky - Over 100,000 investments - Not enough time to do adequate analysis, even for the pros |

| Market Timing | - Fun and exciting to bet - If you are right a lot more than wrong, get rich quick |

- More risky and difficult than SS - Need to be correct >75% time - 1 in 8 "professional" timers beats the markets 3 years in a row |

Asset Allocation

Spreading money in your portfolio between different types, or classes, of investments

Asset Allocation accounts for between 75% - 90% of long-term portfolio performance

Gary Brinson, Brian Singer and Gilbert Beebower “Determinants of Portfolio Performance II: An Update, Financial Analysts Journal, May/June 1991

Major Asset Classes I Use

Cash

Short-Term Bonds

Intermediate / Long-Term Bonds

High-Yield (junk) Bonds

International Bonds

Emerging Markets Bonds

Large-Cap Value

Large-Cap Growth

All/Mid-Cap

Small-Cap

Technology

Biotech / Health Care

Micro-Cap

Internet

International / Global All-Cap

Emerging Markets

Real Estate

Tangibles

Money Management Essentials

| Essentials | Mistakes |

|---|---|

| Have a plan – Educate yourself or work with an advisor | Unrealistic goals, too general, undefined or unrealistic |

| Implement your plan | Procrastination |

| Pensions and investment earnings get taxed | Ignoring effect of taxes |

| Insure low frequency, low probability, high loss events | Having no insurance against death disability or liability |

| Diversification is a must: Don't significantly overweight | Over-weighted in current "fad" of investing: Tech stocks, real estate, employer |

| Inflation 3% long-term average minimum last 75 years | Ignoring inflation |

| Investment decisions based on: diversification, sticking to a plan | Making investments decisions based on emotions: fear & greed |

| Know what advice you need: good advisors are valuable | DIY – In order to save money |

| Know your ability and tendency to take risk: translate to portfolio | Too conservative or too aggressive |

| Diversification is essential | Concentration not diversification |

| Asset Allocation – Only reasonable long-term strategy | Not understanding Asset Allocation |

| Nobody can do it reliably, not even the "experts: | Trying to time markets |

| Cash is only one asset class | Too much cash |

| Someone who is an expert in one area does not make them an experienced investor | Over influenced by friends, family, TV, salesman, etc |

| By the time you hear about it, it is too late or illegal (insider info) | Placing bets on "hot companies" |

| There are no guarantees in investing: You pay to lose your money slowly (eg cash and annuities) |

Wanting everything guaranteed |

| If you and/or your spouse are not disciplined, hire an advisor | Lack of discipline |

| Long-term investing is a marathon, not a sprint | Wanting immediate results |

| Set reasonable expectations | Wanting something for nothing |

| Be cautious who you rely on for financial assistance | Over-reliance on others: inheritances, family marriage, lottery, home, etc. |

| Short-term: nobody knows where the market is going | Thinking that any one person knows where the market is going |

How risky is cash in the bank?

Is your “guaranteed” money really safe in the bank?

| $100 Principle x 4% Interest $104.00 EOY |

$4 Earned Interest 35% Marginal Tax Rate $1.40 Lost to Taxes |

$102.6 After Tax Value 3.5% Inflation $3.59 Lost to Inflation |

|---|---|---|

| $104.00 Nominal End of Year Balance -$1.40 Taxes Due -$3.59 Inflation $99.01 Real Value at the End of the Year |

||

Conclusion: Real loss of 1% in first year. Over 9.5% loss in ten years and 30% in 35 years!

You pay for certainty: no risk = no real return

American Taxes & Financial Planning

Living in Switzerland

Income taxes

FBARs

Gift & estate taxes

IRA accounts

2nd and 3rd Pillars

529 Plans

Over 90% of tax problems for overseas Americans can be avoided by timely filing of FBARs and tax returns as accurately as possible

Regardless of how “simple” you think your financial life is, it is generally more complex than you think

Income Taxes – Filing a US Federal Tax Return

All Americans with even small amounts of income need to file a tax return:

Generally with earned income over $10,000 ($20K married filing jointly)

More than $1000 in unearned income (higher if over age 65)

Self-employment income over $400

Church employee with income over $108

A return must be filed even if taxes are not owed (penalties can be high for non-compliance) – “I did not know the rules” is not generally an accepted answer by the IRS

The following link will help: http://www.irs.gove/Individuals/Do-You-Need-to-File-a-Federal-Income-TaxReturn%3F

Income Taxes – Types of Income Reportable

From employment (including benefits such as)

school fees

car allowance

some expenses reimbursed

employer contributions to non-qualified pension plan

Self-employment - Schedule C

Rental income (regardless of where rental property is located)

“Passive” income

Pensions - US and foreign, private and government

Interest, dividends, capital gains, market-to-market for PFICs

Other

Distributions from trusts or similar vehicles

Certain insurance and annuity contracts

Sale of collectibles: coins, art, metals, etc

Income Taxes – Miscellaneous

Inheritance received from a “covered expat” is taxable to the beneficiary

inheritance or gift(s) of over $100K cumulative in one calendar year from a non-US person (who is not a covered expat) is reportable (form 3520) but not taxable

Ownership of over 10% of a foreign corporation: 5471, different reporting for different ownership thresh-holds

FBARs

Financial Bank Account Reporting Form – Changing to FinCEN 114

Must file electronically now by June 30th every year, no extension

Must file if over $10K at any point cumulatively in any calendar year

Must file if signatory authority over accounts, even if no beneficial ownership

Traditional IRA Accounts

Individuals with earned income (not excluded) can contribute $5500 in 2013 ($6500 if over age 50)

Contributions are deductible, regardless of income level, if not contributing to a US qualified pension plan

Assets grow US tax deferred

Switzerland has the right but not the obligation to tax these accounts

IRA accounts can be opened at many US institutions for residents of Switzerland

Other IRA Accounts

Roth IRAs

Conversion to a Roth may be interesting if you are overseas and have no income (eg as a trailing spouse married to a non-US taxpayer)

SEP IRA

Can be used by self-employed overseas individuals

Inherited IRA

Make sure you understand minimum distribution requirements, penalties are up to 50% (not an overseas issue)

Converting to Roth IRAs

Traditional

Employer 401K

IRA Withdrawals

Age 59 1/2 for distributions without penalties

Age 70 1/2 for required minimum distributions

Misc IRA Info

Assets will not pass through probate; though difficulties can arise for non-US beneficiaries

Non-US beneficiaries may be able to receive distributions without any US taxes if lump sum taxation paid in Switzerland

Children can open IRA accounts and fund them if they have earned income

2nd and 3rd Pillar Accounts

Income is reportable annually in US

Contributions are not tax deductible in the US

Common error: Employer contributions are not reported as taxable income

To avoid double taxation, track your US tax basis in 2nd and 3rd Pillar accounts

Many 3rd Pillar and 2nd Pillar “libre passage” investments are PFICs

Don’t contribute to 3rd Pillar or excess 2nd Pillar “buybacks” if the result is a lower Swiss tax bill offset by a higher US tax bill

If you have money “stuck” in a 3rd Pillar, leave it in cash – USB from 2014 is forcing its US clients to do this anyway

529 Plans

Married couple can give up to $140,000 to a 529 plan in first year (5x Annual Gift Limitation)

529 Plan assets grow US tax free if used for qualified education

Over 350 foreign institutions qualify (eg. Lausanne Hotel School, University of Geneva)

http://www.savingforcollege.com/eligible_institutions/

PFIC – 3 Ways to Account

Sections 1291 through 1297 of US income tax code: Rules are essentially to discourage US people owning these types of investments

Most US people should avoid PFICs at all costs

Form 8621 must be filed each year (very cumbersome)

http://www.irs.gov/instructions/i8621/ch01.html3 ways to report income:

Get the fund to report under US reporting rules: segment interest, dividends, capital gains distributions, etc

Mark to market each year. Gains are taxed in year, losses not used to offset, future gains must be above high water mark (QEF Election: Qualified Electing Fund)

Gains pro-rated over several years of holding, taxes, interest and penalties due for all previous years

Money and Children

Money is still a taboo subject: Many families find it easier to talk about the facts of life than about money

Spend money and time in ways that are consistent with your values

There is no “one” correct way

Your children will be strongly affected by your actions

Follow your instincts

Educate yourself on what several “professionals” think

8 Steps to Raising Successful, Generous and Responsible Children

Encourage a work ethic

Get your money stories straight

Facilitate financial reflection

Be a charitable family

Teach financial literacy

Spend time and money in ways that are consistent with your values

Be aware of and moderate your extreme money tendencies

Engage in difficult financial discussions

Book: The Financially Intelligent Parent: Gallo & Gallo

Tips for Parents

Kids see and emulate more than we are aware of: Are your money actions in-line with values you would like to teach?

Don’t tie allowance to household chores

Give responsibility early:

Allowance: save, spend, invest, charity

Bank accounts

Credit card (for convenience)

Employment

Encourage & support: savings, investing, charity and spending

Financial training does not end when kids leave home…

Use the right language: Don’t say “we can’t afford it”

Include children in money discussion: Ensure they know how much things cost

Be open with your spouse

Emphasize doing your best rather than being the best

Don’t argue regularly about money in front of your children

Useful Resources

“The Financially Intelligent Parent” - Gallo & Gallo

Money Savvy Generation Website: http://www.msgen.com/assembled/home.html

Estate Planning

What happens to your assets when you or your spouse dies?

Estate Planning - Checklist

Do you have a will? Has it been updated?

Have you prepared an estate planning letter?

Do you know what will happen if you or your spouse die overseas?

Do you have enough life insurance?

Who will take care of minor children (raising them and finances)?

Do you have a listing of location of all valuable papers, assets, accounts, passwords?

If you have a business - continuity plan?

Insurance documents - updated including beneficiaries?

Do you have durable health care power of attorney, general power of attorney?

Do you have a living will?

Have you made your wishes known: heirlooms, location of burial, type of service, donations to charity, etc?

Do you need a trust arrangement: For sizable estates or take care of minor children?

5 Steps to Preparing Heirs

Assessing your wealth transition plan

Taking action on plan deficiencies

Preparing Heirs

The Heir’s self-preparation responsibilities

Continuing evaluation & measurement

Book: Preparing Heirs - Williams & Preisser

Government and Employee Benefits

Read the fine print – know your rights

http://www.ssa.gov/

http://www.bsv.admin.ch/

If you receive expat benefits: They don’t remain forever – schooling, health care, housing, car, etc.

Common Financial Questions

How much money do I need to retire?

How much money should I be saving towards retirement?

What age can I afford to stop working?

What percentage of my portfolio can I afford to spend in retirement?

Should I put all of my money into an annuity at retirement?

Should I invest in stocks?

How much emergency cash should I have?

In what currency should I invest?

Should I invest in real estate?

Retirement – Calculating How Much You Need

Life expectancy

Taxes

Inflation

Investment return

Spending needs

Percent covered by government & company pensions

Retirement Calculator

| White Lighthouse Retirement Calculator | Inputs |

|---|---|

| AnnualI Income Goal (Today) – After Tax | $100,000 |

| Percent of Income Covered by Govt + Company Pension | 40.0% |

| Years Until Retirement | 25 |

| Number of Years Required After Retirement | 30 |

| Inflation | 3.00% |

| Portfolio Yield - Before Taxes | 7.00% |

| Portfolio Yield - After Taxes - Before Retirement | 5.60% |

| Portfolio Yield - After Taxes - In Retirement | 5.25% |

| Average Tax Rate on Investment Earnings - Before Retirement | 20% |

| Average Tax Rate - In Retirement | 25% |

| When you retire, your annual income needs (from your portfolio) will be | $125,627 |

| In 25 years, we need a lump sum of (PV of Growing Annuity Stream) | $2,663,609 |

| Current Savings | $500,000 |

| Amount Needed to Save Each Year to Reach Goal | $13,711 |