To view this presentation in PDF format, click here.

ACA Town Hall

Estate Planning for Overseas Americans in Switzerland

May 10, 2012

Webster University Geneva

Jonathan Lachowitz

Certified Financial Planner™ –Investment Advisor

This presentation is not meant as legal, tax or financial advice to any individual. This is a general explanation of cross-border issues between the US and Switzerland. You are strongly recommended to seek the advice of a professional who understands your specific circumstances before relying on any of the information in this presentation. There may be mistakes and regulations may change or not apply in some circumstances. The presentation may be circulated but should be appropriately cited if used in a professional setting.

IRS Circular 230 Disclosure: Any tax advice in this communication is not intended or written by the author to be used, and cannot be used, by a client or any other person or entity for the purpose of avoiding penalties that may be imposed on any taxpayer.

Jonathan Lachowitz – CFP®

Certified Financial Planner ™ & Investment Advisor –Switzerland and US

MBA 1996 – Finance & Marketing – New York University’s Stern School of Business

Specialized in cross-border financial planning, especially with overseas US citizens in Switzerland

US & Swiss National

Founded White Lighthouse Investment Management – 2006 – Lausanne

Owner JJK Investment Management (Registered Investment Advisor) in US

Serving ~100 clients in personal financial planning and asset management

Develop & teach personal finance courses at IMD

Board Member of ACA – American Citizen’s Abroad (Geneva)

Board Member of SFPO (Swiss Financial Planning Organization – Bern)

Email: lachowitz@white-lighthouse.com/ www.white-lighthouse.com

Outline

Estate Planning Checklist

Government Forms – Starting Estate Settlement

Financial Accounts

Estates & Gifts – US Taxes

US – Swiss Estate Tax Treaty / EU Regulations

Government & Employer Benefits

US Expatriation & Giving Up a Green Card – Estate Planning

Tips for American Expats

Being a Smart Consumer & Choosing a Professional Advisor

Conclusion

Estate Planning – Checklist

Do you have a will? Has it been updated? Is it valid where you are living?

Have you prepared an estate planning letter?

Do you know what will happen if you or your spouse die overseas?

Do you have enough life insurance?

Who will take care of minor children (raising them and finances)?

Do you have a listing of location of all valuable papers, assets accounts, passwords?

If you have a business – continuity plan?

Insurance documents - updated including beneficiaries?

Do you have durable health care power of attorney, general power of attorney?

Do you have a living will?

Have you made your wishes known: heirlooms, location of burial, type of service, donations to charity, etc?

Do you need a trust arrangement: for sizable estates, to take care of minor children, to avoid probate, other reasons?

Government Forms – Starting Estate Settlement

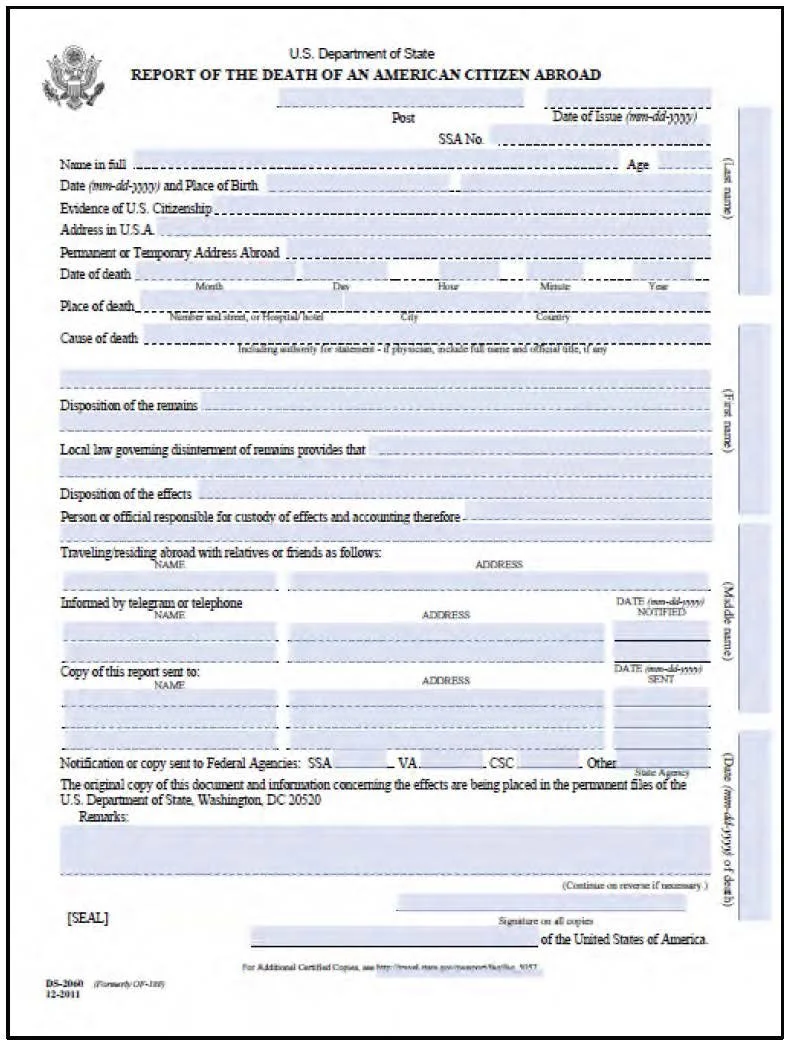

Consular Report of Death of American Abroad – DS 2060

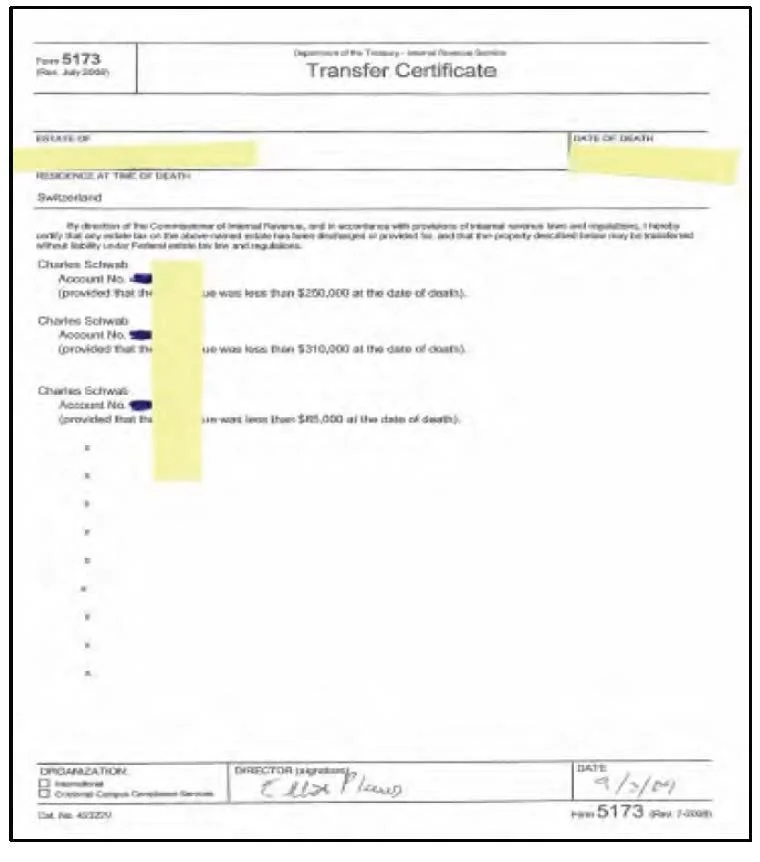

IRS Transfer Certificate 5173

US Estate Tax Return

Settling an overseas estate can easily take 6 months, a year, or longer

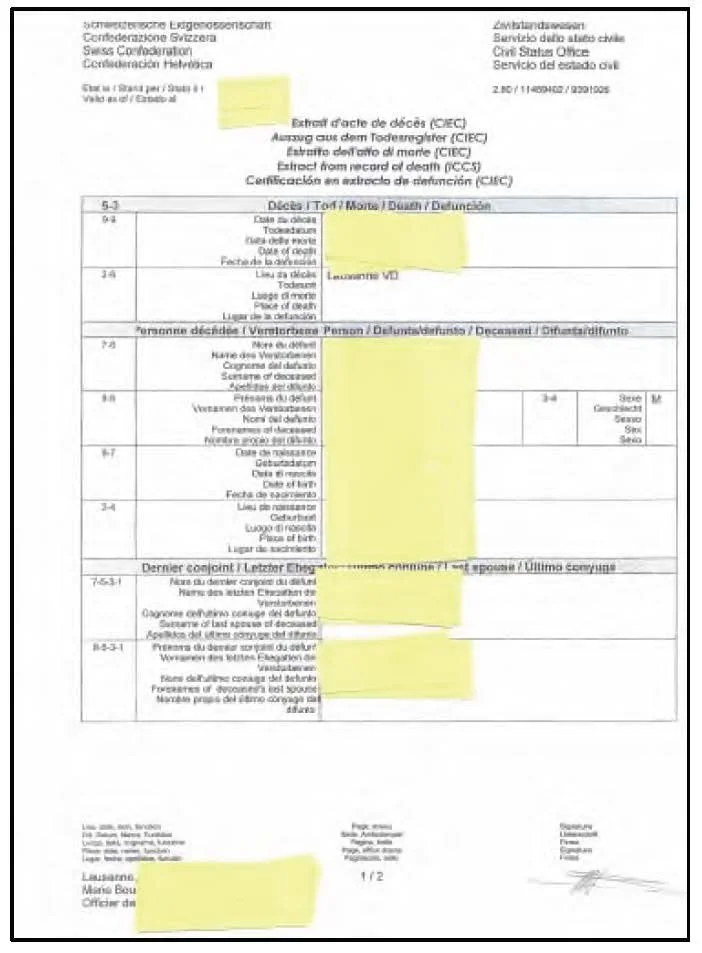

Swiss - Death Certificate

Requesting Consular Report of Death of US Citizen Abroad

Contact US Citizen Services at the closest Embassy or Consulate

Based on foreign death certificate, which must be received first

http://travel.state.gov/travel/tips/emergencies/death/death_3878.html

http://bern.usembassy.gov/service/death-of-an-american-citizen-abroad.html

http://travel.state.gov/travel/tips/emergencies/death/death_1204.html

Call the Embassy at 031-357-7011 for the latest requirements to request this form

More info can also be obtained from email to citizeninfo@state.gov

Generally 20 certified copies of Consular Report of Death (DS 2060) are given “free of charge” upon the initial request

Sample DS 2060 Overseas Death Certificate

US Estate Tax Return

IRS Form 706 – Only 28 pages

US Estate (and Generation Skipping Transfer) Tax Return

http://www.irs.gov/pub/irs-pdf/f706.pdf

Generally the responsibility of your executor

Many CPAs do not have experience filling this return

IRS Form 706 Instructions: http://www.irs.gov/instructions/i706/index.html

File within 9 months of death of decedent

2012 Required filing if Gross Estate is over $5.12 million estate tax 35%

Drops to $1 million in 2013 & 55% estate tax unless Congress acts

IRS Transfer Certificate: Form 5173

Written request to:

IRS SB/SE Estate Tax Group 1205

820 First St NE, Suite 730

Washington, DC 20002Include:

DS-2060 Report of Death of American Citizen Abroad

Signed affidavit listing worldwide assets at time of death and any taxable gifts after 1976

Copy of decedent’s last will and testament in English (may need to be a notarized copy)

Filing of local country estate tax return if required in local country

Expect 3 months for a response

Check with IRS to see if requirements have changed at time of request, especially with respect to documents that may need to be notarized

Sample IRS Form 5173

Misc Info

NRA owning over $60,000 in “us situs” assets will owe estate taxes at highest federal rate

NRA gifting US assets, no gift taxes

One US spouse can inherit unlimited assets with no estate tax due, from another US citizen spouse

Non-citizen spouse inheriting from US citizen subject to exemption limits and estate tax, can defer with a QDOT

Financial Accounts

What happens to financial accounts when someone dies?

How does a financial institution find out about the death of an account holder?

Pitfalls to plan for:

joint accounts

first named on account is often important

credit card

US IRA Accounts

Are your beneficiaries up-to-date?

401K Plans

Inherited IRA rules are different than “regular” IRAs in terms of distribution schedules and amounts; depends on who inherits; age of decedent and age of beneficiary

Rollover IRA

Special rules for Roth IRA and inherited Roth IRA. Generally 5-year-rule must be met to keep these “tax free”; heirs must withdraw within 5 years or distribute over their lifetime

Swiss lump sum taxation available for Swiss resident; though generally only advisable for non-US persons

Beneficiaries on IRA Accounts

Are your beneficiaries up-to-date and in proportion to your desires? Don’t disinherit recently born children or grandchildren.

What if a non-American inherits an IRA?

Spousal IRAs and inherited IRAs have different distribution requirements. [Generally driven by account value, age of decedent, and age of beneficiary.]

Transfer on Death Forms

Many US brokerages allow this election; it will be executed upon death and avoids probate and overrides any election in a will.

US brokerages will generally follow US state laws and will not allow this election if you live outside the US (so they don’t conflict with local laws)

Can be an effective planning tool before leaving the US

Life Insurance – Review

Are your beneficiaries up-to-date?

Do you have enough coverage for the right event? Income replacement versus estate planning?

Is your plan a US-qualified insurance plan?

Who owns the policy and will it be in the decedent’s estate?

Could you benefit from a life insurance trust?

US Accounts Owned by Non-US People

Investment accounts or real estate

Possibly inherited from US person

Planning for US Estate Tax for non-US persons

Generally personal investment company inside a structure (trust or company)

Could you benefit from a trust or other structure?

In many cases, yes

Best to discuss with a qualified attorney

Estates & Gifts – US Taxes

What happens to your assets when you or your spouse dies?

What limitations do I have on gifts?

Chart on next pages - Credit to Prudential Financial

Part of the Prudential Insurance Company of America and is not considered legal, accounting or tax advice

General Gift Tax Situs Guidelines for Non-Resident Aliens by Family or Property

| Type of Property | Subject to Gift Tax | Not Subject to Gift Tax |

|---|---|---|

| General Rule | Real and tangible personal property situs in US at time of transfer |

Real property outside the US |

| Real Property | Real property, i.e. land, building, fixtures, and improvements located in the US |

Real property outside the US |

| Tangible Personal Property |

Property physically in the US Note: Cash/currency whether in US dollars or foreign currency, is treated as tangible property and will incur gift tax on gifts made within the US |

Property outside the US |

| Intangible Person Property |

None. Note: This is in contrast with estate tax where such property located in the US is subject to estate tax |

Intangible personal property, i.e. stocks, mutual funds, bank, brokerage, and fiduciary accounts even if located in the US |

| Life Insurance | Gifts of cash by non-resident alien to make premium payments are gifts of cash and subject to gift tax (unless limited to annual gift tax exclusion) |

Policy insuring non-resident alien or another can be transferred without a gift tax and does not need to worry about 3-year pullback rule |

General Gift Tax Situs Guidelines for Non-Resident Aliens by Form of Property

| Type of Property | Included in the Taxable Estate | Non-included in the Taxable Estate (or exceptions to the rule) |

|---|---|---|

| General Rule | Assets situated within the US or titled therein must be fully disclosed on Form 706 NA. |

Assets not situated within the US generally do not have to be disclosed |

| Real Property | Real property, i.e. land, building, fixtures, and improvements, located in the US |

Real property outside the US |

| Tangible Personal Property |

Property physically in the US cash/currency is considered tangible property (although most forms of monetary instruments are not) and is taxable if in US |

Tangible property in the possession of the foreign national if only temporarily visiting the US |

| Bank, Brokerage & Fiduciary Accounts |

Funds held by US banks or other financial institutions, if used in conjunction with a US trade or business; funds held in brokerage accounts; deposits with domestic branches of foreign banks are also subject to this trade or business requirement |

Savings accounts, checking accounts or certificates of deposit issued by a US bank if not used in conjunction with a US trade or business; funds held in a US bank custody account; funds deposited in a foreign branch of a US bank |

| Qualified Retirement Plan |

Assets held by Plan Administrators representing work for a US company |

|

| Stock | Shares issued by a US corporation regardless of situs |

Shares issued by a foreign corporation regardless of situs |

| Life Insurance | The value of a policy on the life of another person (i.e. the interpolated terminal reserve) issued by a US licensed insurance company and owned by the decedent |

The proceeds from an insurance policy on the life of the non-resident regard- less of the insurance company's country of origin |

| Annuities | The value of any annuity issued by a US insurance company on the life of another |

Annuities where issued by foreign insurance companies |

Summary of Estate & Gift Tax

| Decedent / Surviving Spouse |

Decedent's Estate Tax Applicable Exemption Equivalent (1) |

Estate Tax Marital Deduction |

Decedent's Interest In Property Held Jointly With Spouse (2) |

Annual Marital Gift Tax Exclusion (3) |

Availability of Gift- Splitting to a Third Party |

Availability of Gift Tax Annual Exclusion (4) |

|---|---|---|---|---|---|---|

| US Citizen / US Citizen |

$5M | Unlimited | 50% | Unlimited | Available | Available |

| US Citizen / Resident Alien |

$5M | Only with QDOT | 100% | $136,000 | Available | Available |

| US Citizen / Non-Resident Alien |

$5M | Only with QDOT | 100% | $136,000 | Not Available | Available |

| Resident Alien / US Citizen |

$5M | Unlimited | 50% | Unlimited | Available | Available |

| Resident Alien / Resident Alien |

$5M | Only with QDOT | 100% | $136,000 | Available | Available |

| Resident Alien / Non-Resident Alien |

$5M | Only with QDOT | 100% | $136,000 | Not Available | Available |

| Non-Resident Alien / US Citizen |

$60,000 | Unlimited | 50% | Unlimited | Not Available | Available |

| Non-Resident Alien / Resident Alien |

$60,000 | Only with QDOT | 100% | $136,000 | Not Available | Available |

| Non-Resident Alien / Non-Resident Alien |

$60,000 | Only with QDOT | 100% | $136,000 | Not Available | Available |

(1) Applicable for 2011-2012

(2) Unless considerations can be substantiated for the non-citizen surviving spouse’s portion

(3) Rates for 2011

(4) $13,000 - 3&4 Indexed for inflation

Situs Rules

| Type of Property | US Citizen | US Resident | Non-Resident Alien |

|---|---|---|---|

| Gift Tax | Worldwide gifts subject to US gift tax |

Worldwide gifts subject to US gift tax |

Gifts of real and tangible personal US situs property subject to US gift tax. Gifts of intangible US situs property (e.g. stock, certain deposits and life insurance) and gifts of non-US situs property not subject to US gift tax |

| Estate Tax | Worldwide property owned by decedent subject to US estate tax |

Worldwide property owned by decedent subject to US estate tax |

US situs property owned by decedent subject to US estate tax |

US Federal Estate Tax – US Citizens

2012 – $5.1 million exemption, 35% estate tax

Married couple (both US citizens) can get full exemption $10.2 million on 2nd to die as long as Estate Tax return is filed. (Historically a trust set-up was often used to accomplish this.)

2013 – $1 million exemption. 55% estate tax unless Congress acts to change it (they probably will but it will probably be late)

Income Tax Rules – Year of Death

Surviving spouse or personal representative should file final tax return

DECEASED with date of death should be written at the top of the return

Full year standard deduction applies, but only itemized expenses and income up until date of death

Medical expenses received and paid up to 1 year after date of death can be treated as having been paid by the decedent for income tax purposes

Income (over $600) after death (in respect of decedent) requires Form 041

Can create some confusion on 1099 forms and other income statements received from banks and brokerage accounts

Form 1030 must be filed i the final tax return is claiming a refund

State Tax returns may need to be filed too (e.g. if Real Property is owned in the US)

In the year of death of one spouse, surviving spouse can use same filing status that year

Surviving spouse may use $500,000 credit against sale of home (instead of $250,000 for an individual) if the home is sold within 2 years of the spouse’s death

Inherited Assets receive a step up in basis (gifted assets retain their original cost basis)

Gifts to non-citizen spouse $139,000 limit per year – estate tax treated like “non spouse” if surviving spouse is a non-American

Non-American owning US assets still only $60,000 exemption

Estate Planning for Non-Citizen Spouse

Non-citizen surviving spouse subject to US Estate Taxes above exemption amount

Non-citizen spouse owning US assets only has a $60,000 exemption from US Estate Tax

US citizen can gift non-citizen spouse $139,000 per year (2012 limit) + $13,000 annual gift limit

QDOT can be formed to defer US Estate Taxes until time of death of non-citizen spouse

Estate Planning for Non-Citizen Spouse QDOT Information

Can be formed post mortem (within 9 months of death, extension can be filed for)

At least one US Trustee who is US citizen or US corporation

Executor must make an irrevocable QDOT election to qualify for marital deduction on Federal Estate tax return (form 709)

If QDOT has equal to or less than $2 million, only 35% can be real property outside the US or else:

Trustee must be a US bank

Individual US Trustee must furnish a bond for 65% of the QDOT assets at the transferors demise or

The individual US Trustee must furnish an irrevocable letter of credit to the US Government for 65% of the value

If QDOT has over $2million in Assets then one of the items 1, 2, or 3 above need to be met

Any property that the deceased spouse transfers to the surviving spouse outside of the QDOT (e.g. beneficiary election, joint tenancy, etc.) may be transferred to the QDOT without estate tax before the estate tax return is due [9 months after date of death with a possibility to apply for a 6-month extension]

Primary requirements for a QDOT is that the surviving spouse can not be the only Trustee

Distributions of QDOT income are not subject to estate tax when made; distributions of principal are subject to federal estate tax

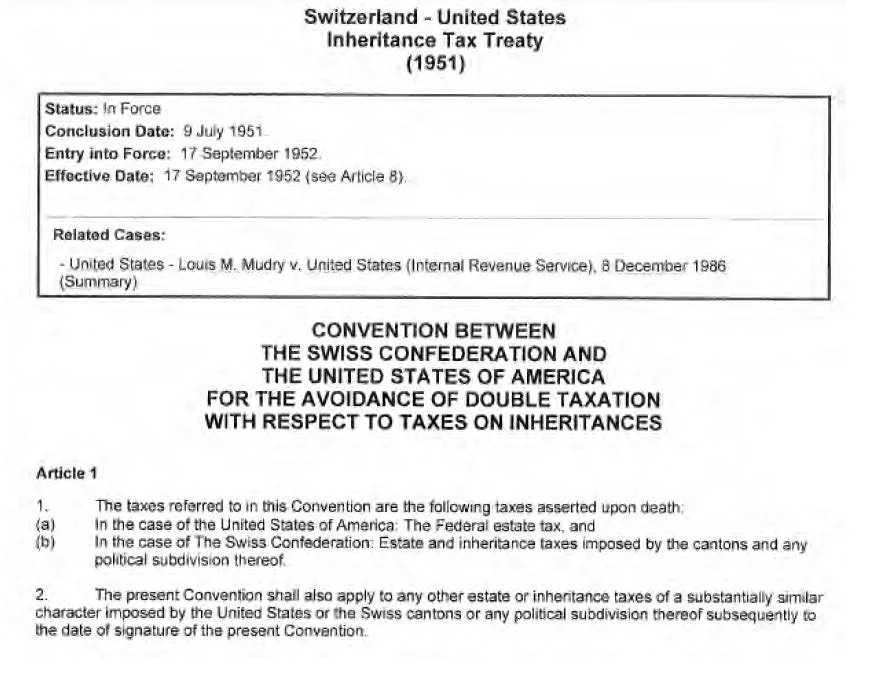

US-Swiss Estate Tax Treaty

Went into force in 1951 – not updated since

Aims to prevent double taxation of estates

Misc Item – Online Assets (1)

How to bequeath online assets?

Gmail will provide emails to an executor upon death

Facebook will allow relatives to close an account or turn it into a memorial page

iTunes license for music can be revoked upon death; all iCloud data is deleted upon death of an owner

5 American states have enacted laws giving an executor rights over a deceased persons social networking sites

Some cases already litigated in the US

Securesafe, a Swiss company, recently acquired Entrustet and allows users to store passwords and setup who can access what information when they die.

(1) Economist article, April 12, 2012, page 76, “Deathless Data”

EU Succession Laws (1)

From 2015, expatriates in all EU countries will have the right to have their country of nationality’s succession laws apply – similar to Switzerland today

An elective statement can be made through a will or European Certificate of Succession

Country of residence estate tax law will still apply

Variable tax rates on estate planning by country and based on “type” of beneficiary

UK, Ireland, and Denmark have opted out of this Brussels IV regulation

(1) Credit to Blevinsfranks Article 11, April 2012, http://www.blevinsfranks.com

Government Benefits & Employee Benefits

Read the fine print – know your rights

US Social Security: http://www.ssa.gov/

Swiss AVS: http://www.bvs.admin.ch/

US Embassy in Bern is a great resource for Swiss/US social security rules

US Social Security & AVS – Highlights

US Swiss Totalization Agreement

http://www.ssa.gov/international/Agreement_Pamphlets/switzrld.html

US Social Security – More generous to non-working spouse

US – WEP

What Happens To US & Social Security When A Decedent Passes Away?

US – Surviving Spouse receives the higher of their own or their spouse’s SS.

US – Dependents may also be eligible (e.g. younger children or disabled dependents)

Swiss AVS – Less generous for surviving spouse

Swiss Taxation of US Social Security

| US Social Security – Gross Benefit | 100 |

|---|---|

| US tax, Limited to 15% Under Article 19(4) | -15 |

| Net Received from US Sources | 85 |

| Exempt Amount Under Article 23(2)(d) | 28.33 |

| Swiss Taxable Benefit | 56.67 |

| Swiss Tax Rate: Assume Maximum Rate of 40% | -22.67 |

| Net After All US and Swiss Income Taxes | 62.33 |

US Expatriation – Estate Planning

Applies to US Nationals

Applies to long-term green card holders – 8 of the past 15 years

Expatriation not necessarily beneficial for US Estate Tax purposes

US Expatriation & Relinquishing Green Card

New rules in affect since June 17, 2008

If

Net worth above $2 million

Average US tax burden for last 5 years is above $147,000 (2011 limit, indexed) or

Fails to certify that they have compiled with all US tax obligations from last 5 years

The 3-year look back has been eliminated which can be an effective planning tool.

Long-term green card holder (8 of the last 15 years)

All property deemed sold at date of expatriation. If gain is above $600,000, then expatriation will be a taxable event.

US Expatriation & Relinquishing Green Card

Some people can escape the rules (dual nationals/accidental Americans)

The exceptions are dual nationals from birth, who have not lived in the US for more than 10 years from the last 15, and persons younger than 18 1/2 who have not lived in the US for more than 10 years.

Estate type tax on any US person who receives a gift (directly or via trust) from a “covered” expat 35% in 2011

Certain deferred tax items not subject to mark-to-market: (Stock options, pension rights, restricted stock units and other deferred compensation, certain tax deferred accounts, and non-grantor trusts), but still subject to US taxes

30% tax imposed on all post-expatriation trust distributions received by covered expat. Could result in 51% next tax on distributions from certain pension plans and retirement accounts.

Procedure to Expatriate

Get a second citizenship in another country

Leave the US

Appear before the US Consul in that country to renounce your US citizenship

File the form 8854, Expatriation Information Statement

Pay the exit tax due, if any

As a covered expatriate, you will be able to visit and stay for certain time in the United States, and the mere fact of being an expatriate does not make you a US tax resident. You still can become taxable in the US under the normal US tax rules.

Tips for Americans Overseas

Get a regular copy of your free annual credit report: +1 877 322 8228

Consider implementing a security freeze to prevent ID theft: http://redtape.msnbc.com/2007/11/now-a-way-to-st.html#posts

Get a regular copy of your US Social Security Statement: http://www.ssa.gov/

File your annual US tax returns – It can now be checked upon passport renewal!

Keep a US credit card with a US address

Keep a US address (for investing, credit cards & possible insurance)

Know what happens if you return to your previous state of residence, especially on state income tax for years you were away

Get a US phone number (Skype, call 800 number for free)

Review life insurance and long-term care insurance in the US

Review a US-based will

Investigate what happens if you were to die while living overseas (Swiss Law different than US)

If you plan to return to the US, work with advisors who are experienced with the US “system” : financial, tax, legal, etc

Travel to the US only on your US passport

Vote in the Presidential elections (federal ok, local elections not advised from overseas)

New voting form, Department of Defense – Federal Post Card application – will affect which elections you can vote in and may affect taxation, at the state level, especially upon return. Some states very aggressive: e.g. Virginia, Maryland, & Massachusetts

I am a US citizen residing outside of the US and I intent to return

I am a US citizen residing outside of the US and I do not intent to return

Check out previous residence: “unclaimed property”

If you are married to a non-American, make sure you know the estate planning and gift tax implications! There are advantages and disadvantages…

Being a Smart Financial Consumer

Investment of your time – even if the subject is not interesting

Together with your spouse or partner

Together with your advisor(s)

Educate yourself

Hiring a professional(s) where a specialist(s) are needed

You will need to pay for most professional advice

Being a good client – Advisors choose you as much as you choose them. Be respect, honest, and timely.

E.g. If you have had 5 new tax advisors in 5 years, the problem may not be the tax advisors

The expat community & advisor community is small

Know your costs

Know your rights and obligations

Advice is not always “right” - Trust, but verify

Comparison shopping

Choosing a Professional Advisor

Do you need a professional advisor(s)? Why?

What are the advisor’s services and do they match your needs? Different titles…

Whose interests do they put first? Are they fiduciary, employee, salesperson?

What are you looking for and what do you think you need?

A financial plan?

An estate plan?

Legal advice? Documents?

Get references from people you trust – Ask the one thing your reference does not like

What licenses, education, registrations do they hold?

What experience do they have? Would you be a typical client?

How does the advisor get paid?

Is their advice objective? How do you know? Are they paid more to sell their company’s products?

Have they been involved in any lawsuits or other disciplinary action?

Do you know how to be a “valued” client?

Gut feel

Concluding Thoughts

Time and education are your best assets

Find professional help when you need it – Hire people who are more qualified than you and expect to pay for personalized advice

Don’t expect government, employer, family or children to take care of informing you; if they do, that’s a bonus – You are in the driver’s seat

Ask good questions

Things change (frequently) stay prepared & educated!