To view this presentation in PDF format, click here.

Financial Independence

Session 2 – Charting Your Course!

June 2007

Jonathan Lachowitz

Financial Planner – Investment Advisor

This presentation is not meant as legal, tax or financial advice to any individual. You are strongly recommended to seek the advice of a professional who understands your specific circumstances before relying on any of the information in this presentation. There may be mistakes and regulations may change or not apply in some circumstances. The presentation may be circulated but should be appropriately cited if used in a professional setting.

Financial Independence Part II: Charting your course!

Agenda

Introduction

Questions to Consider

Money Management

Investing Fundamentals

Understanding Risk

Group Work – Presentations

Saving and Investing

Conclusion

Part 1 – Introduction & Review – Welcome Back

“People who like this sort of thing will find this sort of thing they like.”

- Abraham Lincoln

Previous Session

How much money do I need to retire?

Factors:

Inflation

Taxes

Life Expectancy

Investment Return

Income Needs

We now have a “number”, probably 7 figures…How do we get there?

Charting Your Course

A combination of saving and investing

A balance between today and tomorrow

Long-term perspective is needed

Many sources

Government Pension

Company Pension

Private Pension

Private Savings

Today we will focus on those areas where you have the most control – saving and investing privately

Discussion Question: How important is money?

Some Famous Money Quotations…

“Money can’t buy happiness, but neither can poverty.” - Leo Rosten

“There is no amount of money in the world that will make you comfortable if you are not comfortable with yourself.” – Stuart Wilde

“While money can’t buy happiness, it certainly lets you choose your own form of misery.” – Groucho Marks

“Whoever said money can’t buy happiness simply didn’t know where to go shopping.” – Bo Derek

“I’d rather be rich and healthy than poor and sick.” – My dad

“This contempt for money is just another trick of the rich to keep the poor without.” - Michael Corleone

“Money can’t buy you happiness, but it’ll let you park your yacht next to it.” - David Gilmour, Pink Floyd

“The real measure of your wealth is how much you’d be worth if you lost all of your money.” - Unknown

“Money is better than poverty, if only for financial reasons.” – Woody Allen

Quotations Continued

The old saying “money can’t buy happiness” has been proven wrong by researchers at The University of Nottingham. A study into lottery jackpot winner – those who have won more than £1 million – found that a resounding 97% of interviewees were just as happy, if not happier, following their big win.

“This planet [Earth] has – or rather had – a problem, which was this: Most of the people living on it were unhappy for pretty much of the time. Many solutions were suggested for this problem, but most of these were largely concerned with the movements of small green pieces of paper, which is odd because on the whole it wasn’t the small green pieces of paper that were unhappy.” – Douglas Adams

“It is the kind of spiritual snobbery that makes people think they can be happy without money.” - Albert Camus

“When it is a question of money, everybody is of the same religion.” – Voltaire

A Word or Two About Money

Money should not be the focus of retirement or life planning….but it is the focus of this session.

Financial freedom does make some choices easier…but freedom of choice is not easy.

Part 2 – Questions to Consider

“The chief value of money lies in the fact that one lives in a world in which it is overestimated.” - HL Mencken

Money or Time?

Are you more likely to die (physically or otherwise) in retirement from boredom or lack of financial means?

Is it more important to you to know what you want to do with your time or how you will finance it?

Buzz Group Questions

How will you spend your time in retirement? (Don’t forget to have something to do when you are financially independent.)

Where do you get your investment advice?

How do you decide when to buy or sell an investment?

How much are you saving each month towards retirement? Percent of income?

What is your biggest fear about investing?

Part 3 – Money Management

“The key to making money in stocks is not to get scared out of them.”

– Peter Lynch

3 Ways to Manage Money

Who read the article?

Before we get into Money Management…A review of some common mistakes and essentials about money…

25 Biggest Money Mistakes (not in order)

Procrastinating about financial decisions

Having goals that are too general, undefined, or unrealistic

Not having a plan or having one that won’t work

Ignoring the effect of taxes in your plan

Going uninsured against death, disability, and liability

Ignoring cost of living inflation in your plans

Being overweighted in the current fad (tech stocks)

Making decisions based on emotion (fear and greed)

Wanting to do it yourself to save money (sometimes)

Being too conservative or too aggressive

Not understanding the concept of asset allocation

Concentration rather than diversification

Placing bets on hot companies (stock tips & speculating vs investing)

Being overly influenced by others (friends & family)

Placing market timing bets (speculating vs investing)

Failure to take profits or cut losses

Idle assets (having too much in cash)

Assuming things will just work themselves out

Demanding immediate results and satisfaction

Wanting everything guaranteed

Lack of spending/savings/investment discipline

Thinking that any person, firm, or magazine knows where any market, or security, is going, and when

Not understanding the many problems with money

Over-reliance on expected inheritances, promotions, business ventures, marriages, winning the lottery, etc

Wanting something for nothing

25 Biggest Money Essentials (not in order)

Educate yourself about investments

Educate yourself about taxes

Educate yourself about inflation

Establish realistic short and long-term goals

Spend within your means

Use insurance appropriately

Involve your spouse and family

Don’t procrastinate over financial decisions

Develop a plan and commit to the process

Avoid the current fads (e.g. dot com stocks, hedge funds)

Deversify (no more than 5% in one stock)

Do not have more than 80% in stocks

Don’t try to “time” any financial market

Determine and invest according to your risk tolerance

Save/Invest systematically - pay yourself first

Have enough cash reserves to handle emergencies

Make decisions logically, not emotionally

Realize that you will have to pay for expert advice

Plan for bad news on inflation and taxes

Make your own decisions and don’t be overly influenced by others (colleagues, friends, and family)

Take profit and cut losses (buy low, sell high)

Don’t have too much in idle assets (cash, money market, CDs, etc)

Take action – don’t assume things will always work out and go your way if you just wait and do nothing

Understand the difference between market timing, security selection, and asset allocation

Realize that no person, TV show, or firm, knows where any stock, or market is going, when, or by how much

Survey Questions

How many of you feel that you are better than average investors?

Do you know your long-term average rate of return on investments? And if that is “good”?

3 Ways to Manage Money

Security Selection

Market Timing

Asset Allocation

Advantages of Security Selection

If you were right, a lot more than you were wrong, then you can make a lot of money quickly. Some stocks have gone up many times in less than a year (e.g. Amazon, Google)

If your bet pays off, you can brag to everyone about what a genius you are

It’s fun and exciting to watch your bets on a daily basis

Problems with Individual Security Selection

It’s too hard, risky, and depends mostly on guesswork

With over 50,000 mutual/investment funds, and 20,000 stocks globally, where do you start?

There isn’t enough time to do an adequate analysis

There are too many qualified people out bargain hunting already - The more people looking, the less bargains

There is too little information available and it is quickly outdated - Only the “insiders” have the information that matters, and they can’t tell anyone because of the insider trading laws

If you get lucky, you can become overconfident, and then lose big the next time around

Advantages of Market Timing

If you were right, a lot more than you were wrong, then you were wrong, then you can make a lot of money quickly. Some stocks have gone up many times in less than a year (e.g. Amazon, Google)

If your bet pays off, you can brag to everyone about what a genius you are

It’s fun and exciting to watch your bets on a daily basis

Problems with Market Timing

It’s even more difficult and risky than security selection

Nobody can predict the future with any degree of consistency

Need to be correct more than 75% of the time to break even with mistakes, transaction costs, commissions, and taxes. (1)

Only 1 in 4 “timers” beat the market two years in a row, and only 1 in 8, three years in a row. (2)

Results of empirical studies also show that only one in 37 mutual funds showed any benefit from market timing. (3)

(1) The New Finance, Robert A. Haugen, page 13

(2) Managing Investment Portfolios, Donald L Tuttle, chapter 13, page 36

(3) Modern Portfolio Theory and Investment Analysis, Edwin J Elton and Martin Gruber, page 36

Advantages of Asset Allocation

It’s investing and not speculating. The goal is consistent long-term good performance that’s worth the risks, rather than spectacular (or disastrous) short-term results.

It’s a proven long-term diversification strategy that balances risks and returns.

It takes guesswork and emotions out of investment portfolio management.

It focuses on the portfolio as a whole, instead of on picking and timing each part separately.

It’s the best way to create a portfolio that will help stay in line with your unique investment objectives.

It’s easy to implement, monitor, and rebalance.

Problems with Asset Allocation

It’s very boring compared to security selection and market timing. Most of the emotional roller coaster is gone.

By spreading your money around, your exposure to the highest performing asset classes is diluted. You’re not going to hit the jackpot, but you’re not going to lose everything either.

Periodic rebalancing is needed. You should also rebalance when there is a change in your life situation.

You have to decide which asset classes to use, and how much. You may have some asset classes you don’t like.

Inexperienced investors don’t understand or like bonds.

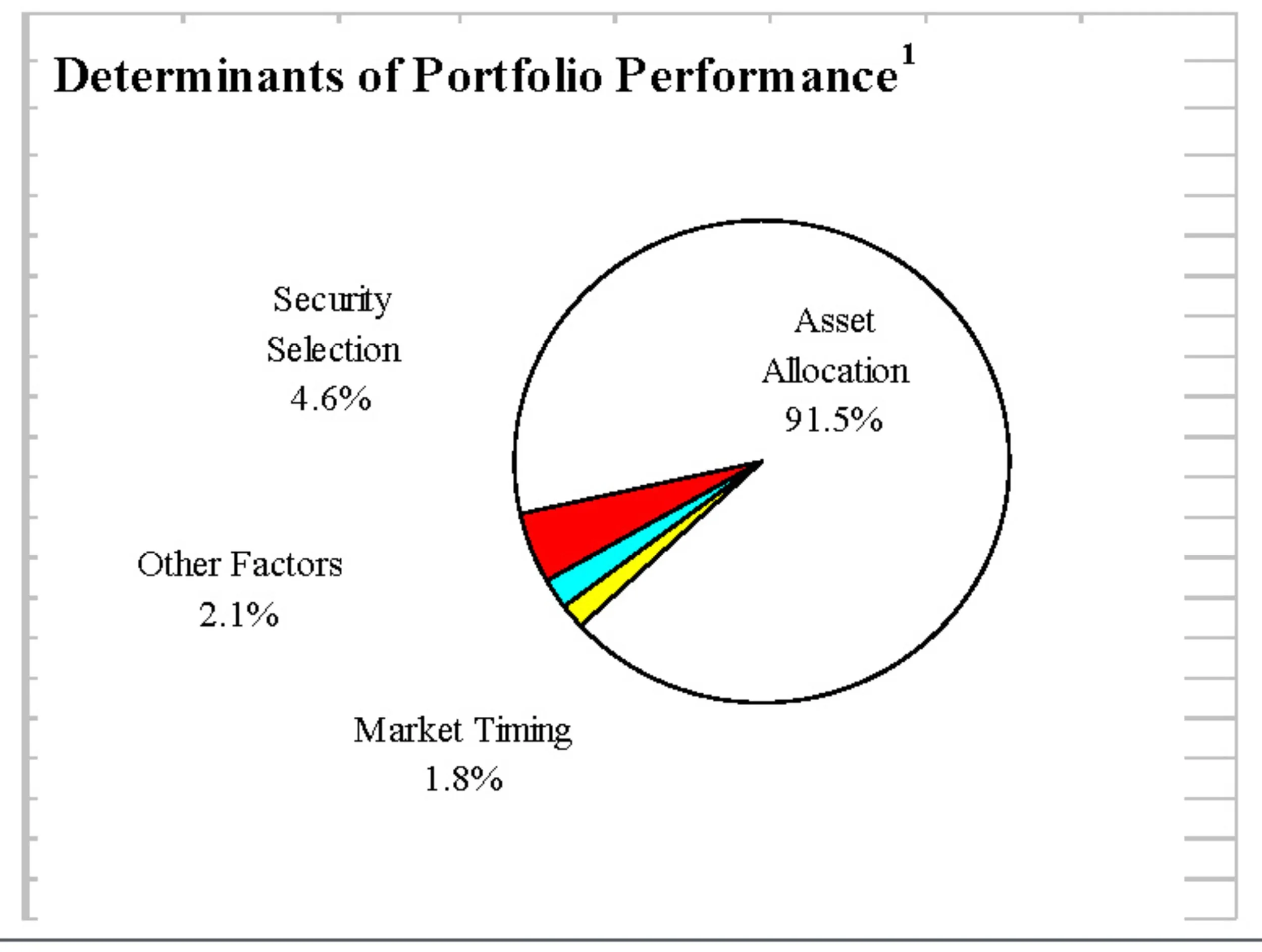

Asset Allocation

Spreading the money in your portfolio between different types, or classes of investments.

Asset Allocation accounts for between 75-91% of long-term portfolio performance.

Gary Binson, Brian Singer, and Gilbert Beebower, “Determinants of Portfolio Performance II: An Update”, Financial Analysts Journal, May/June 1991

What is Asset Allocation - Review

Part A Basic Asset Class Allocator

Instructions – Fill in the 4 input cells (with yellow background) below under the column “Choices”

Your 5 Asset Class Allocation

| Input Selection | Choices | Labels | Asset Class | Percentage |

|---|---|---|---|---|

| Risk Categoery | Conservative | Take Survey Below | Cash and Cash Equivalent | 10.0% |

| Portfolio Income Need |

0% | Percent | Income (Government & Corporate Bonds) | 32.5% |

| Investable Assets | 200,000 | US Dollars | Large Cap-Growth Stocks | 25.0% |

| Income | 100,000 | US Dollars | International & Emerging Market Stocks | 12.5% |

| Age | 40 | Years | Aggressive Growth Stocks: eg Small Cap, Sectors, Tangibles | 20% |

| Total | 100% |

Note: This guideline is for educational purposes only and can be used as a basis of discussion with your own advisor(s). You should make investment decisions only with the assistance of your own personal financial advisor(s); this information here should not be seen as personal advice.

Part 4 – Investing Fundamentals

“Our favorite holding period is forever.”

- Warren Buffet

“In this business, if you’re good, you’re right six times out of ten. You’re never going to be right nine times out of ten.”

- Peter Lynch

Investment Planning - Process

Focuses on your long-term goals

Identify your risk-return profile

Decide on a plan: Security Selection (stock pricing), Market Timing, and/or Asset Allocation

Incorporate assets not directly under your control (eg company pensions)

Implement, monitor, and revise plan as needed

Investments

Is anyone in the class willing to share their best or worst investment experience?

Basic Investment Vehicles

Stocks

Bonds

Cash deposits

Derivatives

Investment Funds are centralized pools of money that have a number of investors, either individuals or other companies. These funds rely on the pooling of resources to invest in higher value investments than the individuals involved in the fund would normally be able to invest in.

Investment Fund Advantages:

Diversification for smaller investment amounts

Can be cost/fee efficient

Leave “professional” management to the professional or use Index funds for relative safety

Easier to manage a portfolio of funds than a portfolio of stocks and bonds

Choosing an Investment Fund – Suggested Criteria

Performance against it’s piers or benchmark over 1, 3, 5 years

Management Tenure

Fee Structure inside the fund

Fee Structure to buy or sell the fund

Minimum investment requirements

Does the fund invest in the same types of investments it is classified as ? (e.g. a small-cap fund holding Google, not good)

Actual performance

Tax appropriateness

Investing Fundamentals

Diversification…A story.

Keep expenses and fees low.

Get professional advice when you need it.

Time value of money.

Be careful, cautious, skeptical: If something sounds too good to be true, it most likely is.

Don’t be greedy.

Be patient.

Often the best learning experiences in investing are when you lose money.

Part 5 – Understanding Risk

“Risk – if one has to jump a stream and knows how wide it is, he will not jump. If he doesn’t know how wide it is, he’ll jump and six times out of ten he’ll make it.”

- Persian, author unknown

Personal Definition of Risk

Who will share your definition of risk with the class?

Part B Personal Definition of Risk

Instructions – Write your own definition of risk. E.g. Risk means losing more than 20% of my investment portfolio

Quotes on Risk

“If you don’t risk anything you risk even more.” - Erica Jong

“What you risk reveals what you value.” - Jeanette Winterson

“Be wary of the man who urges an action in which he himself incurs no risk.” - Joaquin Setanti

“Take calculated risks. That is quite different from being rash.” - George S Patton

“The policy of being too cautious is the greatest risk of all.” - Jawaharlal Nehru

“There are risks and costs to a program of action. But they are far less than the long-range risks and costs of comfortable inaction.” - John F Kennedy

“A lot of people approach risk as if it’s the enemy when it’s really fortune’s accomplice.” - Sting

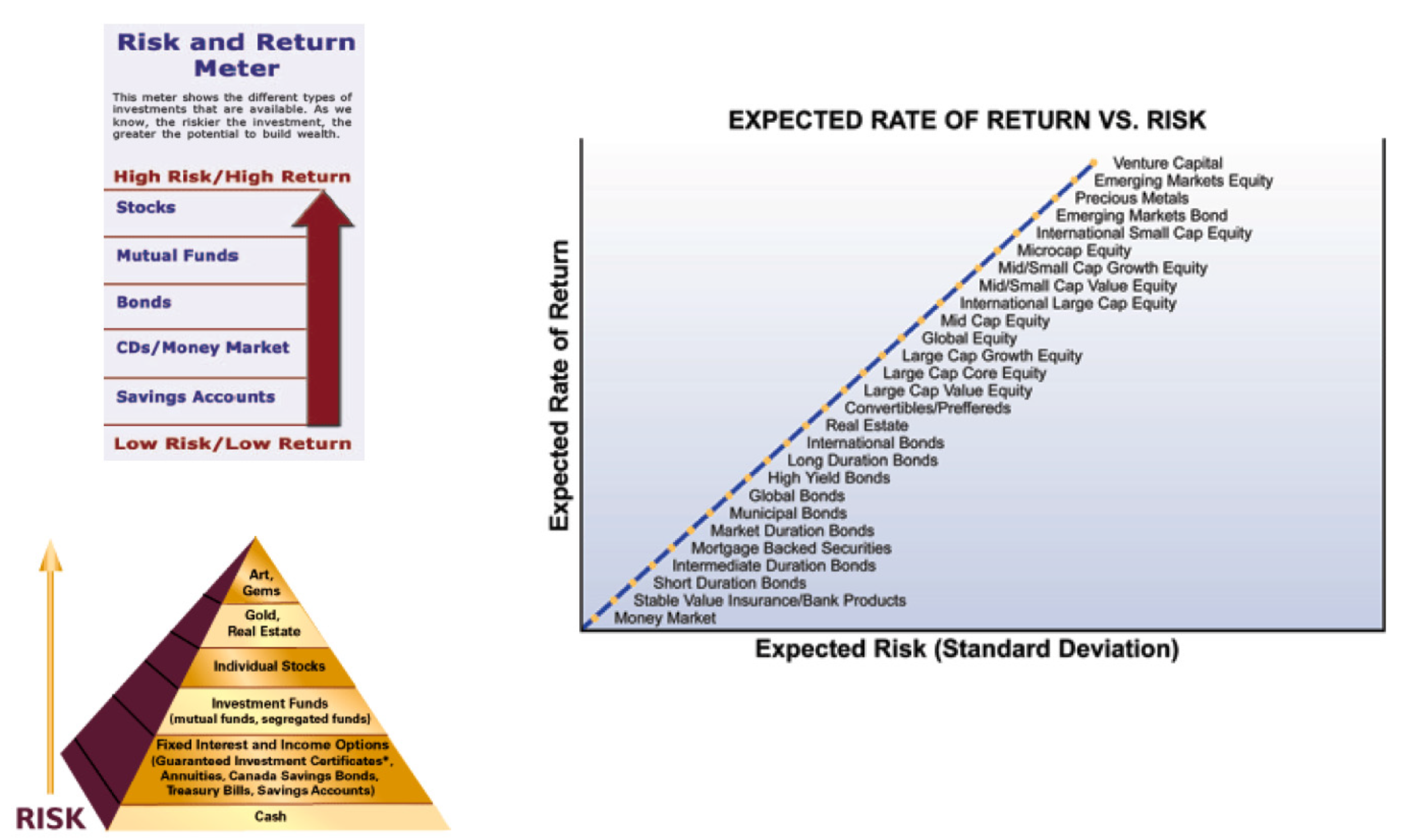

Risk

Defined in terms of Standard Deviation

Riskier assets will deviate more over time

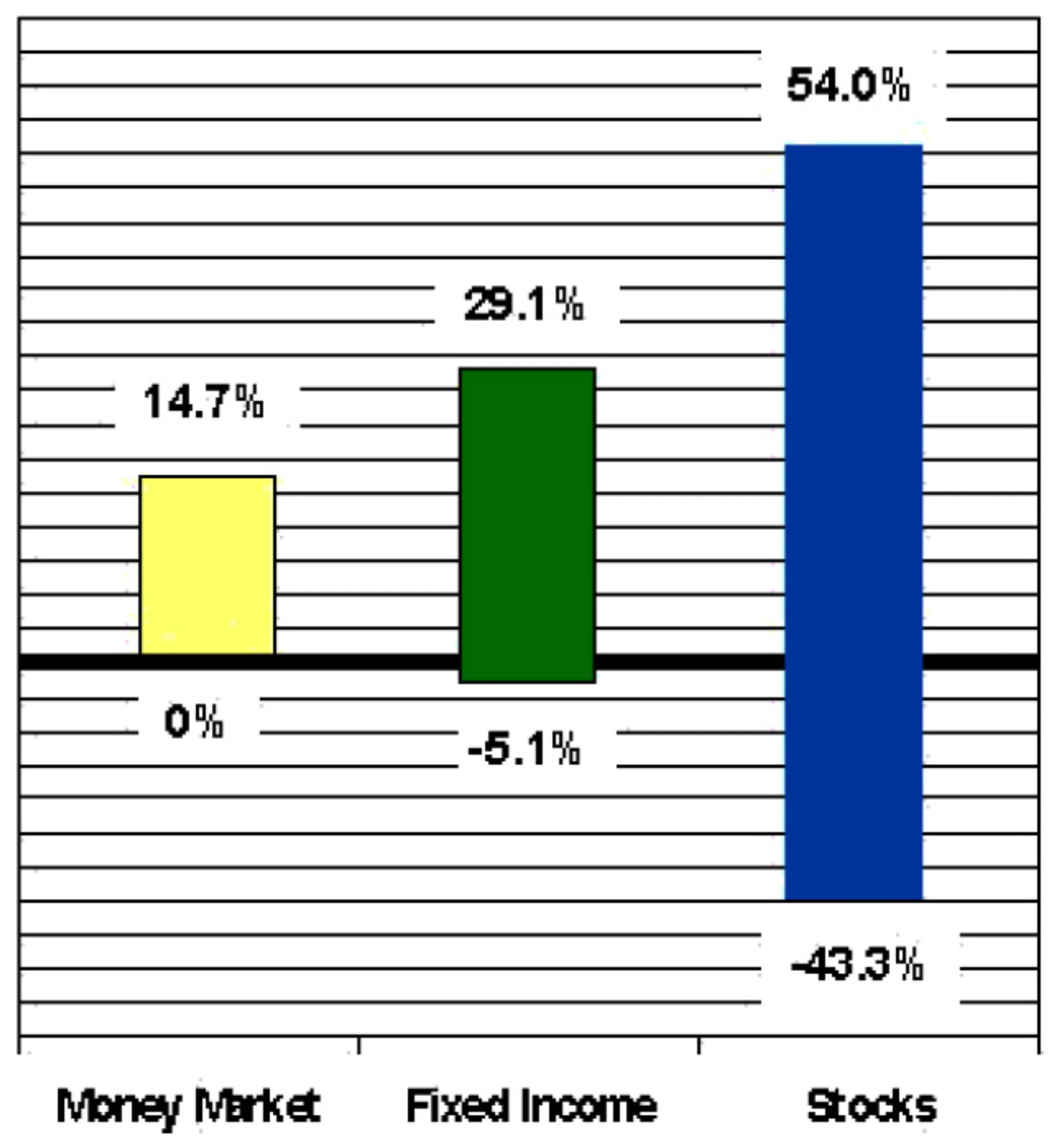

Range of 1 Year Returns Since 1926

Risk vs Expected Return

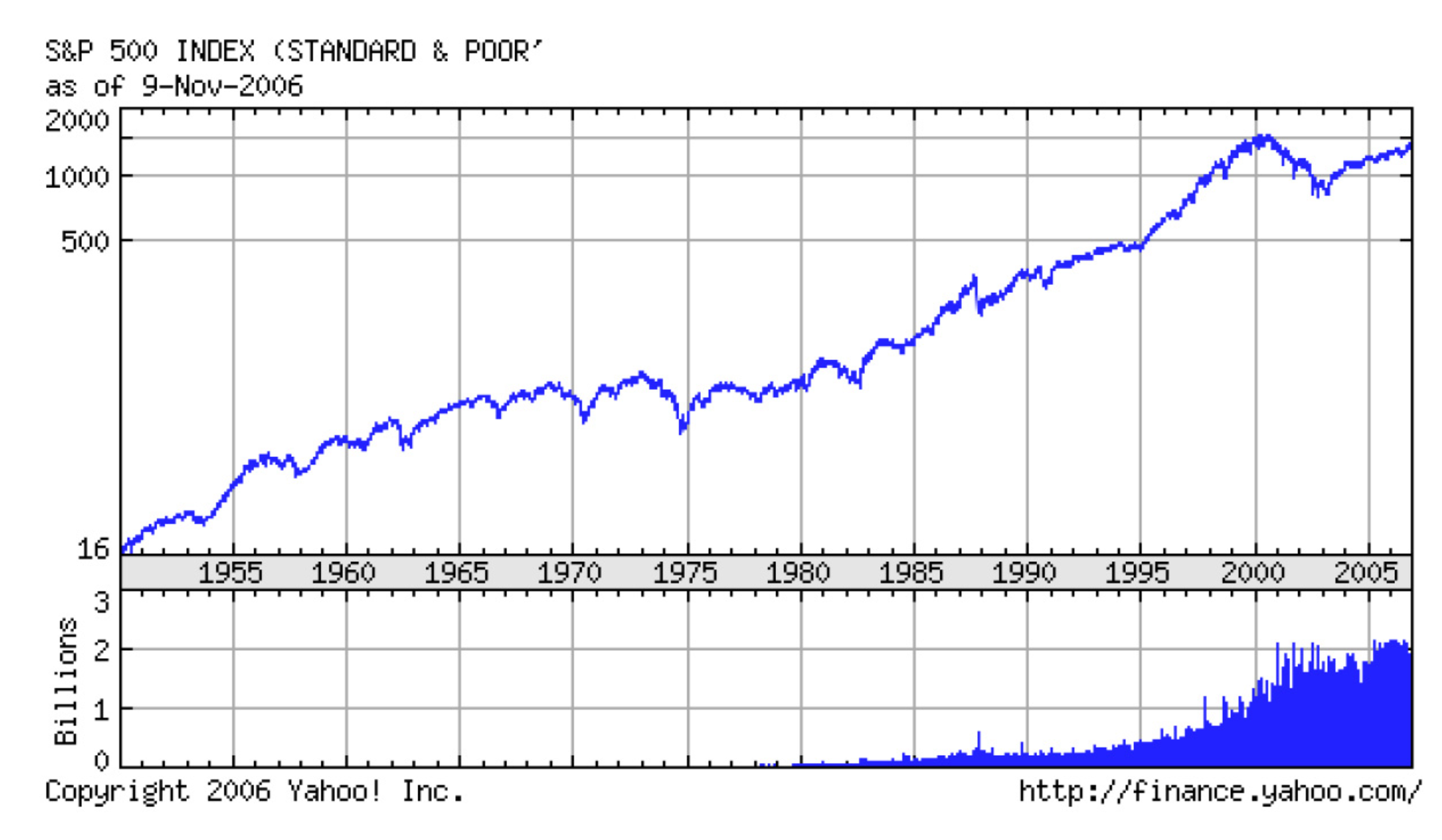

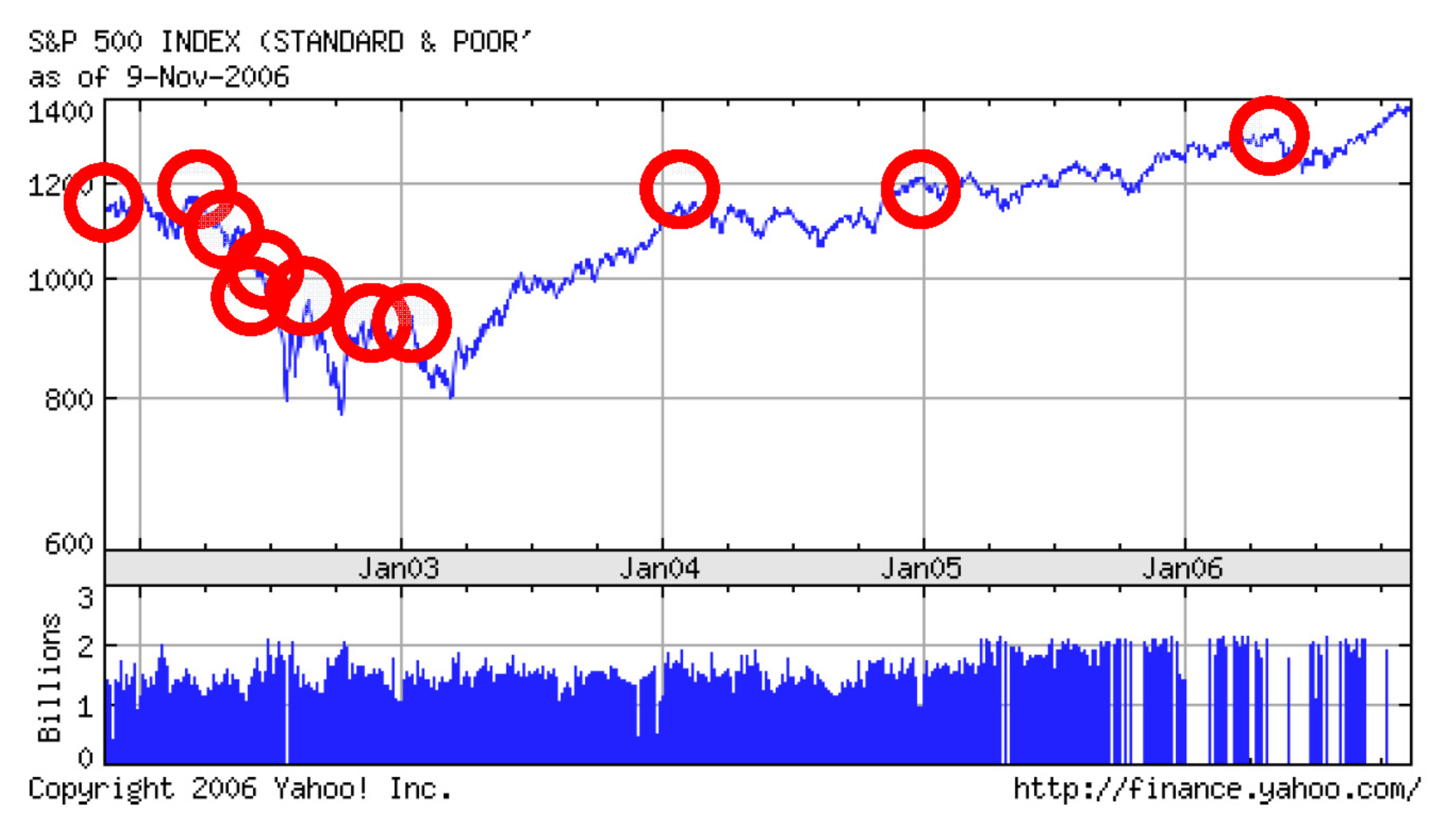

S&P 500

The S&P 500 Index comprises of 500 companies that account for 85% of the dollar value of all NYSE stocks. It is a broader and more representative average than the DOW but both move in tandem most of the time. The S&P 500 Index does not include dividends. It is capitalization weighted, meaning that stocks with the highest value (number of shares outstanding multiplied by the price per share) have the greatest affect on the index.

S&P 500 – 55+ Years

S&P 500 – Last 5 Years

Part 6 – Group Work – Building a Basic Investment Portfolio

“Individual commitment to a group effort – that is what makes a team work, a company work, a society work, a civilization work.” - Vince Lombardi

“There is no such thing as a self-made individual. You will reach your goals only with the help of others.” - George Shinn

5 Groups

Cash

Bonds

Large Cap Growth Stocks

International Equity / Emerging Markets or Country Specific

Aggressive Growth: Sector Funds, Tangibles, etc.

Group Instructions

Each group has to work as a team to choose an investment from one of the classes and explain to the class the rational for their choice.

Cash

Bonds

Growth Stocks

International Equity / Emerging Markets or Country Specific

Aggressive Growth: Sector Funds, Tangibles, Etc.

Several websites are available from your browser, here are a few:

morningstar.com

screen.morningstar.com/FundSelector.html?fsection=ToolScreener

swissquote.ch/index/index_funces.e.html

Each group has to choose 2 investments to build our portfolio and tell the class why they chose the investment and why the class should invest in it.

Asset Allocation - Group’s Choices

Part A Basic Asset Class Allocator

Instructions – Fill in the 4 input (with yellow background) below under the column Choices.

Your 5 Asset Class Allocation

| Input Selection | Choices | Labels | Asset Class | Percentage |

|---|---|---|---|---|

| Risk Categoery | Conservative | Take Survey Below | Cash and Cash Equivalent | 10.0% |

| Portfolio Income Need |

0% | Percent | Income (Government & Corporate Bonds) | 32.5% |

| Investable Assets | 200,000 | US Dollars | Large Cap-Growth Stocks | 25.0% |

| Income | 100,000 | US Dollars | International & Emerging Market Stocks | 12.5% |

| Age | 40 | Years | Aggressive Growth Stocks: eg Small Cap, Sectors, Tangibles | 20% |

| Total | 100% |

Note: This guideline is for educational purposes only and can be used as a basis of discussion with your own advisor(s). You should make investment decisions only with the assistance of your own personal financial advisor(s); this information here should not be seen as personal advice.

Part 7 – Saving and Investing

“The right to private property meant at the same time the right and duty to be personally concerned about your own well-being, to be personally concerned about your family’s income, to be personally concerned about your future. This is hard work.”

- Mikhail Khodorkovsky

Solving for Some Numbers

How much money do I need to save each month/year to meet my retirement goals?

If I have a lump sum of X, how much can I afford to spend each year until I run out of money.

Back to Retirement Calculator - Part 2

Savings

Investment

How much money do I need to save each year?

| White Lighthouse Retirement Calculator | Inputs |

|---|---|

| Annual Income Goal (Today) - After Tax | $100,000 |

| Percent of Income Covered by Govt + Company Pension | 10.0% |

| Years Until Retirement | 10 |

| Number of Years Required after Retirement | 25 |

| Inflation | 3.00% |

| Portfolio Yield - Before Taxes | 7.00% |

| Portfolio Yield - After Taxes - Before Retirement | 5.60% |

| Portfolio Yield - After Taxes - In Retirement | 4.90% |

| Average Tax Rate on Investment Earnings - Before Retirement | 20% |

| Average tax Rate on Investment Earnings - In Retirement | 30% |

| When you retire, your annual income needs (from your portfolio) will be | %120.952 |

| In 10 years we need a lump sum of (PV of Growing Annuity Stream) | $2,334,996 |

| Year | 2007 |

| Retirement Year | 2017 |

| Year Portfolio Runs Out | 53 |

If I save X each year, how much will it be worth when I retire?

| White Lighthouse – Future Value – Inflated Savings | Inputs |

|---|---|

| Annual Savings Amount – Year 1 | $33,757 |

| Current Savings / Investment Balance | $250,000 |

| Years Until Retirement | 20 |

| Portfolio Yield - Before Taxes | 7.00% |

| Inflation (applies to annual savings amount) | 3.00% |

| Portfolio Yield - After Taxes - Before Retirement | 5.60% |

| Average Tax Rate on Investment Earnings | 20% |

| Future Value of Current Savings | $743,393 |

| Future Value of Annual Savings | $1,189,76 |

| Future Value of Total Savings | $1,933,069 |

| Annual Savings could be substituted with a deposit today of: | $400,083 |

Will my savings be enough?

| White Lighthouse Retirement Calculator - Lump Sum | Inputs |

|---|---|

| Current Savings | $250,000 |

| Annual Income Goal (Today) - After Tax | $84,000 |

| Government and Company Pension | $70,000 |

| Years Until Retirement | 0 |

| Number of Years Required After Retirement | 25 |

| Inflation | 3.00% |

| Portfolio Yield - Before Taxes | 5.60% |

| Portfolio Yield - After Taxes - Before Retirement | 5.60% |

| Portfolio Yield - After Taxes - In Retirement | 20% |

| Average Tax Rate on Investment Earnings - Before Retirement | 20% |

| Average Tax Rate on Investment Earnings - In Retirement | 20% |

| When you retire, your annual income needs (from your portfolio) will be: | $14,000 |

| In 0 years, we need a lump sum of (PV of Growing Annuity Stream) | $249,735 |

| Positive # = Savings May Be Enough / Negative #, Savings Not Enough | $265 |

| Year | 2007 |

| Retirement Year | 2007 |

| Year Portfolio Runs Out | 2032 |

A Word (Or Two) About Precision

No one knows what the future holds

You or your spouse may pass away, end up in a nursing home, or strike it rich in a business venture, win the lottery, or get an unexpected inheritance

Nobody knows what your expenses will be

Inflation and taxes won’t be constant

Risk and rates of return won’t be constant

Numbers in the reports are just extrapolations, not predictions

Government benefits may be reduced

Company may get sold or go bankrupt and reduce or not honour pension commitments

The goal is to spot trends and balance risk

Investment Portfolio

Learn more about asset allocation

Work with a trusted professional(s) if you can

The 5 asset class model that we built together is a starting point

Don’t expect long-term average annual returns, after taxes and fees, to be too high. 7% is a reasonably good year when inflation is low

Part 8 - Conclusion

“I believe the true road to preeminent success in any line is to make yourself master in that line. I have no faith in the policy of scattering one’s resources, and in my experience I have rarely if ever met a man who achieved preeminence in money making…Certainly never one in manufacturing…Who was interested in many concerns.”

- Andrew Carnegie

Charting Your Course

A combination of saving and investing

”In the old days a man who saved money was a miser; nowadays, he’s a wonder.” - Author UnknownA balance between today and tomorrow

Take all advice with perspective and skepticism – especially from someone who has something to sell (TV Advisors, Myself, etc)

”The economy depends upon as much on economists as the weather does on weather forecasters.” - Jean Paul KauffmannLong-term perspective is needed

Many source - use them all

Government pension

Company pension

Private pension

Private savings

Concluding Thoughts

Time and education are your best assets

Are you saving enough?

Save early and often – Time Value of Money is a Miracle

Einstein misquotes: A lot of stuff like, “Compound interest is the greatest mathematical discovery of all time”, “The most powerful force in the universe is compound interest”Are you expectations realistic?

Remember risk vs reward – There is no such thing as a free lunch

Keep fees and expenses low

Find professional help when you need it

Understand the difference between gambling and investing

Don’t expect government, company, family or children to take care of you: You are in the driver’s seat

Financial independence sessions should be a starting point…And present more questions than answers

Don’t look at your portfolio often & things change. Be prepared!